Economic activity in the Mena region continues to be dominated by low oil prices and geopolitical uncertainty, writes the team at MUFG Bank.

Lower for longer oil prices are testing oil exporter’s government finances, leading to ongoing spending cuts which is taking a toll on economic activity. Meanwhile, oil importing countries have not been able to take full advantage of low oil prices as they are facing the spillover effects of the civil wars and conflicts in the region, insecurity caused by terrorist attacks, as well as lower remittances, grants and foreign direct investments (FDI) due to the impact of low oil prices on GCC countries.

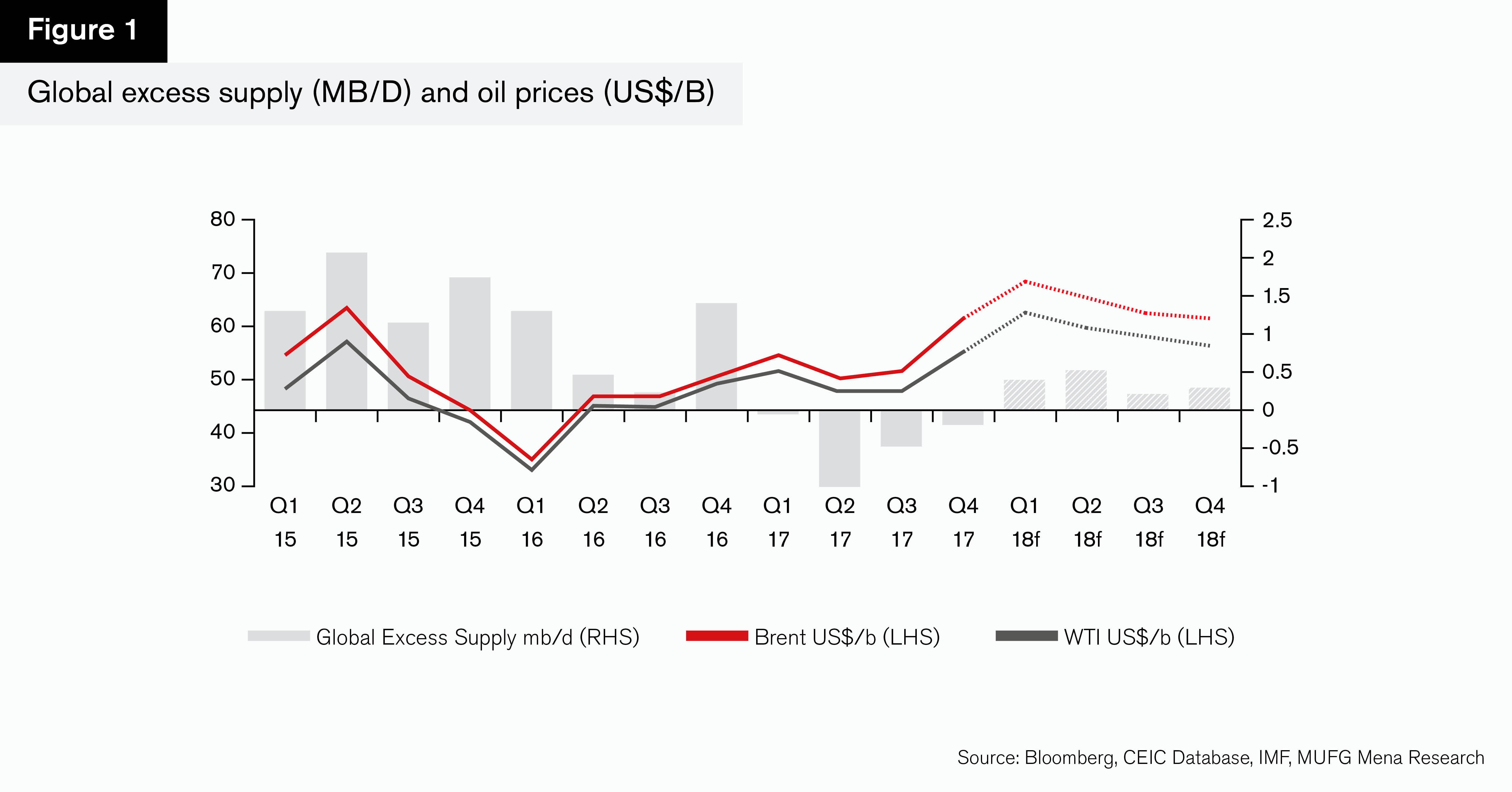

“The bullish momentum in oil prices that we have witnessed throughout 2017 looks, in our view, to be now running somewhat out of steam for multiple reasons,” explains Ehsan Khoman, head of research and strategist for MUFG Bank in Mena. “Firstly, we anticipate

re-emergence oil market imbalances (mainly owing to higher shale production). Secondly, there has recently been increased levels of short covering from money managers and thus more bearish premia now priced into markets. Finally, we expect a wind down in geopolitical risk premia that was a key driver of higher oil prices last year. As such, our econometric models point for Brent and WTI, to average, US$64.4/b and US$59.3/b, respectively, for 2018 as a whole,” he adds.

Although oil prices have witnessed a marked improvement over the last year following the Opec and major oil producers production cut agreement back in November 2016, which have eased the impact on fiscal and current account deficits, the adjustment process is far from being done. We take comfort however, on the composition of fiscal consolidation plans that are being designed, which aim to reduce the negative impact on growth. Efforts on reining in current expenditures include limiting growth of public sector wages and reducing energy subsidies. Also, GCC governments are prioritising capital expenditures to focus on the quality and efficiency of project spending. In conjunction, plans aim to raise non-oil revenue collections, primarily through corporate taxes, import duties and the implementation of VAT, are all accompanying efforts to contain spending.

“Whilst most GCC countries have sufficient savings to cushion a sizable shock, the prolonged period of low oil prices is testing available buffers, highlighting the risks associated with continued dependence on hydrocarbon revenues. Policymakers are continuing to reassess their medium term spending plans and are pragmatically addressing fiscal vulnerabilities from rapidly eroding buffers and high budgetary breakeven oil prices. Even as the GCC economies are expected to grow at a modest pace, policymakers are preparing for a sustained period of low oil prices and reassessing their medium-term fiscal plans. Most GCC countries have outlined ambitious diversification strategies and are embarking on detailed reform agendas, but implementation should be accelerated, particularly to exploit the current stronger global growth momentum,” notes Elyas Algaseer, MUFG Bank’s Co-Head for Mena.

“Attending to growing financing needs in a lower oil price environment is driving the GCC states to increasingly diversify their sources of financing with our economic models suggesting that the cumulative gross financing needs could amount to US$69.3bn for 2018 for the GCC region, and US$149.8bn for region between 2018-22,” highlights Shunsuke Suzuki, MUFG Bank’s regional head for Mena.

“GCC countries have the capacity to finance their deficits and investment programmes for two key reasons: (i) they have accumulated significant savings in the last 15 years, which could be tapped to finance deficits and investments; and (ii) their public debt to GDP ratios are low and moderate (bar Bahrain), making it easy to raise debt on international markets at favourable interest rates. Furthermore, the impact of ongoing fiscal consolidation measures relative to the size of the adjustment necessary to prevent a potential deterioration in credit worthiness may be insufficient in some GCC countries – indeed, any delays or policy reversals may keep ratings under pressure in the vulnerable countries of the GCC region, namely, Bahrain and Oman,” he concludes.

Outside the region, global growth continues to be robust and broad-based, driven by a long-awaited cyclical recovery in manufacturing trade and investment, and this is further being accelerated by US tax policy adjustments. On the negative side, we expect the US to increase its use of trade restrictions in the near term, particularly to rebalance trade with China however this can quickly spread to many other countries. Though we do not expect trade wars, it’s a possibility that cannot be ruled out with confidence.

“For the Mena region, the strengthening global economy represents an opportunity for regional countries to utilise trade as an avenue for growth and expand the range of exports beyond oil and gas. This opportunity, combined with increased digital innovation aimed at streamlining processes, reducing inefficiencies and operational costs for financial institutions and corporates, and improving transparency, all point towards trade finance business in Mena remaining on the upward trajectory in the near term,” notes Kersi Patel, MUFG Bank’s head of trade finance for Mena.

“While the importers and exporters in the Middle East region may have been slower in adopting digitisation than their counterparts globally, we are now seeing increased interest in this area not only from the corporate sector but also from the government sector which has traditionally been very conservative. The infrastructure built by Dubai Trade in this field compares very favourably with the progress made by the globally leading trade facilitators and this will be of big advantage for UAE-based importers and exporters in connecting to global digitised trade networks once they start evolving. MUFG Bank is the leading bank globally by the number and value of digitised trade transactions being currently concluded via TSU BPO. We continue to build on this leadership position in close collaboration with a wide range of industry players and regulators globally, and aim to be at the forefront of this exciting new development in the trade finance industry,” concludes Patel.