Insurance is widely acknowledged as an important enabler of trade; this article from AIG looks at how trade finance and trade credit insurance have specifically helped empower trade, demonstrated via recent case studies.

Banks, and the companies they fund, need insurers and brokers with a deep understanding of trade finance that can also tailor solutions and structures to fit their specific requirements, notes Scott Ettien, EVP Financial Solutions, Trade Credit Practice Leader for North America at Willis Towers Watson. Insurance partners that have a track record of supporting trade finance – both vanilla and complex – including through previous economic cycles, can also better identify potential weak spots in structures, helping protect financiers through challenging times, he adds.

Trade finance case study: insuring media trade receivables

Having the trade finance expertise to underwrite a wide variety of trade risks, in addition to the ability to table its own funding, allowed AIG to support a working-capital provider to break new ground with a media trade receivables securitisation.

The international media and technology industry is mired by a complicated supply chain, with money passing between multiple, interconnected layers of buyers, sellers and agencies based in diverse jurisdictions every time an advertisement appears in print or digital media.

These firms are often able to settle their suppliers’ invoices faster than expected, making traditional working capital products less effective. For others, invoices are settled later than expected, creating higher levels of working capital uncertainty among media sellers over when they will be paid for their services. Harnessing data responsibly can greatly alleviate this issue. Notably, the money that flows through the media supply chain typically ends up owed by large advertisers that are household names and highly creditworthy.

For FastPay, a financial technology platform that specialises in the global media and tech industry, being able to offer payment certainty to bigger media buyers and sellers represented a fresh business opportunity – provided it had the right structures and funding, and an insurer willing to stand behind investors. AIG was able to support FastPay to overcome these challenges.

The result was an externally rated receivables securitisation programme with a first tranche of US$80mn, towards which AIG provided its Excess of Loss Trade Finance Insurance Policy as well as senior funding for the facility, which sat alongside and enhanced FastPay’s bank financing. AIG could add value here as traditional bank funding was restricted in terms of the jurisdictions in which it could be used and the advance rates available. The rating was also backed by AIG’s longstanding ability to provide effective back-up servicing for such structures.

“This is a great example of AIG empowering trade,” says Marilyn Blattner-Hoyle, Global Head of Trade Finance for AIG. “We were able to provide insurance cover against a highly nuanced risk with tech-enhanced visibility of the invoice pool, but then also complement FastPay’s bank financing options with our own AIG funding.”

“We needed partners with an insurance tech background as well as the tools and infrastructure to service the complex media ecosystem,” says FastPay President and COO Secil Baysal.

AIG’s expertise in trade finance structures, the technology/data that underpins these and its ability to offer both insurance and its own capital meant it was uniquely placed to support FastPay as it looked for new growth opportunities, according to Baysal. AIG’s global reach also meant it was able to underwrite and fund in locations that not all banks or insurers could accommodate.

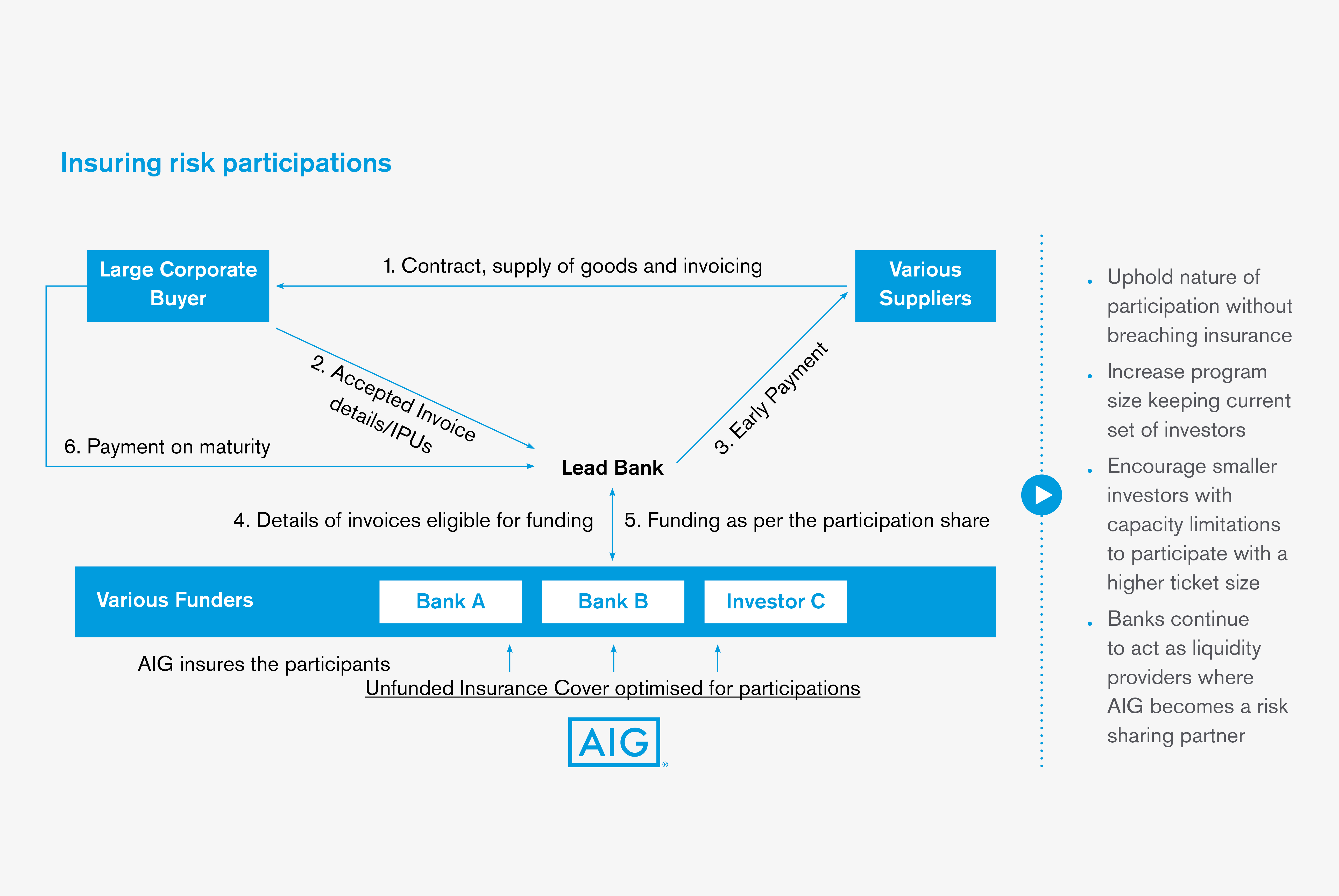

Helping programmes grow: underwriting participations

Insuring bank participations works, and still upholds the nature of a participation.

Banks looking to participate (rather than lead) in a trade finance transaction raises a new dynamic of being one step removed from the obligor. Nevertheless, for such participant banks, internal capacity constraints, coupled with capital efficiency, often enforces the need to approach the insurance market. These banks may find limited options available, however, when it comes to securing an insurance partner that is willing and able to understand the participant bank role in these transactions and underwrite underlying non-payment risk. That pool shrinks further when transactions involve bigger limits on single obligors, more complex structures or a large number of geographically scattered buyers and suppliers.

With supply chain finance being a key growth area for banks (both in terms of leading and participating), AIG has seen a string of recent deals involving participations. In one recent example, AIG insured an international bank’s participation in a global payables programme that another major bank was leading for a large corporate where there were capacity constrains in the market. AIG’s Trade Finance Insurance protected the participating bank from the risk of non-payment by the obligor in the supply chain finance programme, under which suppliers are paid upon acceptance of their invoices by the buyer who is not required to repay the lenders for almost another year. AIG’s expert knowledge of the participation structure, industry and the buyer were critical in the success of the deal.

AIG’s insurance participation in payables programmes like this can also encourage banks and investors to participate with a higher ticket size, helping programmes to grow in a sustainable, secure manner.

In this case, using insurance from AIG allowed the participating bank to improve returns on their risk-weighted assets. This is because it replaced the risk of the obligor with that of AIG, which carries a higher credit rating than the obligor. The participation by AIG’s client was bigger than usual for such transactions and the overall deal included the financing of invoices from more than 170 suppliers across three continents. Where margins and capacity are tight, having the option of using AIG’s Trade Finance Insurance as an effective risk mitigant for this participation made the difference, allowing the bank to secure a risk participation ticket.

Autonomy and security: non-cancellable trade credit cover

Partnering with an insurer that has the capability to commit to trade credit limits, even during volatile times, empowers companies with strong credit and robust risk management in place to maintain their trade flows and protect important customer relationships.

In sectors such as energy, where supply chains are vulnerable to oil price moves and margins can be thin, affordable trade credit insurance is considered essential. Insurers are however required to regularly review credit limits on their clients’ customers and, in the case of traditional trade credit policies, may from time to time reduce or remove those limits to reflect changing risk in the wider environment.

One fuel distributor purchased AIG’s Non-Cancellable Trade Credit Policy this summer following a string of limit reductions by its previous trade credit insurance provider. Having used traditional trade credit insurance for 20 years, this client believes limit changes were starting to disrupt the firm’s trading relationships with key buyers as well as creating additional work for their credit control team.

In a fiercely competitive industry where winning a customer can take as long as a year, having to tell a new customer sometimes after only a month that their credit facility had been cut was becoming frustrating, according to the company’s Head of Transactional Services. “We were strongly motivated at the time to think outside the box,” he says.

With AIG’s Non-Cancellable Trade Credit Policy, the company is now reassured that if it is given a one-year credit limit, that limit will remain in place for the entire year. This has given its sales team more freedom and confidence in their negotiations with prospective customers, resulting in a tangible uptick in sales over the past few months to some buyers, its Head of Transactional Services says. AIG’s competitive premiums were another draw, helping ensure those sales are profitable, he adds.

Because AIG’s Non-Cancellable Trade Credit Insurance involves a level of risk-sharing between AIG and the policyholder, the onus falls on policyholders themselves to carefully assess the risk of offering credit to a specific buyer and to decide whether to sell to that firm – something that the fuel distributor has found to be empowering. AIG’s Non-Cancellable Trade Credit Policy is therefore available only to firms that can demonstrate they have strong credit and risk management processes in place.