Singapore has been rocked by the sudden downfall of two major oil traders. The collapses of Hin Leong and ZenRock – and serious allegations of fraud – have left banks on edge, despite efforts by regulators to discourage de-risking from the sector. John Basquill examines what went wrong, why banks are nervous, and whether technology could help illuminate oil trading’s darker corners.

Hin Leong was founded in 1963, and over the following decades grew to become one of Asia’s largest fuel trading houses – until, in April 2020, its operations came to a shuddering halt. Chairman and founder Lim Oon Kuin revealed on a call with investors the company had suffered US$800mn in undisclosed losses in the futures trading market, and that oil set aside as collateral for lending had also been sold.

Only a fortnight later, news emerged of difficulties at ZenRock, another of Singapore’s independent fuel traders. In early May, HSBC filed a court application to have the company placed under judicial management. Its accusations of fraudulent activity immediately prompted a police raid on the trading house’s Marina View headquarters.

Though Hin Leong and ZenRock’s demise was sparked by a historic crash in oil prices – itself in part a response to plummeting demand due to the Covid-19 pandemic – concerns have not been limited to the fuels sector. Notably, in March, lenders were left with exposures of US$600mn after the collapse of commodities trader Agritrade International.

With banks at risk of having to write off loans – particularly where single trades were financed several times over – firms are finding it increasingly difficult to access fresh lines of funding.

“Financing is effectively coming to a halt across commodity types,” says Baldev Bhinder, managing director of Singapore law firm Blackstone & Gold. “I don’t think that is helpful for anyone – the banks or the economy.”

“The oil crisis has sucked up liquidity from the market, and cumulatively the banks appear to be quite jittery in their lending patterns,” Bhinder tells GTR.

Regulators in the country have sought to reassure lenders that the oil trading sector remains resilient, despite the twin pressures of low oil prices and a significant decline in global demand.

The Monetary Authority of Singapore (MAS) is urging banks not to take a blanket approach to the sector, and continue lending where safe to do so.

“In their credit risk management, banks are expected to apply judicious credit assessments on individual borrowers and not rely on broad-based sector de-risking,” a spokesperson for the regulator tells GTR. “We note that banks in Singapore continue to lend to firms in the oil and gas sector.”

The plea follows an MAS statement issued on April 21 reminding banks “not to de-risk indiscriminately”.

But for banks active in the country, the situation is not necessarily that straightforward. A source familiar with the Hin Leong collapse says some banks are already responding by carrying out a review of how their commodities facilities work across the globe.

“You learn a lot from a fraud crisis,” says the source, who requests not to be identified. “There has been a temporary halt on everything except the most necessary lending – not because banks can’t afford to fund traders but because a lot of these shocks may not have worked their way through the supply chain, and so there are still worries about companies’ financial health.”

Of the international banks with exposure to Hin Leong, the three largest are believed to be HSBC, ABN Amro and Société Générale.

ABN Amro said in its Q1 financial results that “a potential fraud case in Singapore” was one of two exceptional files accounting for €460mn in impairments.

“The corporate loan book is diversified and exposures to high-risk sectors such as offshore, diamonds and trade and commodity finance have been reduced in recent years, although more de-risking is clearly necessary,” it said.

A spokesperson for ABN Amro says the bank never discusses individual client situations nor discloses client names, but adds a review is ongoing into the activities of its corporate and institutional banking activities.

HSBC’s Q1 filings report that its expected credit loss was US$3bn, a year-on-year increase of US$2.4bn, due to “a significant charge related to a corporate exposure in Singapore” as well as the impact of coronavirus-weakened oil prices. The bank declined to comment when contacted by GTR.

A spokesperson for Société Générale confirms it is a lender to Hin Leong, but says it has no exposure to ZenRock. They add the bank “will remain committed to the trade commodity finance sector, including in Asia”.

What went wrong?

Though the initial impetus for Hin Leong’s collapse came from its admission of undisclosed losses, brought to a head by the oil price crisis, the source says several examples of fraudulent practices have since emerged.

They say it is now apparent the company inflated its figures and built up leverage by creating fake trades alongside its legitimate activity.

“We’ve also seen multiple sales of the same cargo,” they add. “You end up with a bunch of banks all trying to lay claim to the same assets, like oil that’s still in storage tanks. In some cases, these sales are fictitious, where the cargo doesn’t exist in the first place.”

Hin Leong has since ceded control to PwC. Its exposure to HSBC reportedly stands at an initial US$600mn, with ABN Amro lending US$300mn and Société Générale lending US$240mn. Local banks DBS, OCBC and United Overseas Bank are exposed by around US$680mn in total.

In the case of ZenRock, the company issued a statement shortly after the Hin Leong incident saying it was not facing financial difficulties itself, despite the oil crisis and pandemic. It claimed to be profitable while dismissing rumours it was “under statutory restructuring/insolvency protection”.

However, in early May, it emerged that HSBC had applied to Singapore’s High Court for the company’s management to be removed. The request was granted, despite efforts by ZenRock to restructure liabilities itself, and further proceedings are expected to take place in July.

An affidavit signed by HSBC’s head of commodities and energy, Kiu Hock Yean, describes “certain trade practices by the company which appear on their face to be shams, or at the very least, extremely suspicious”.

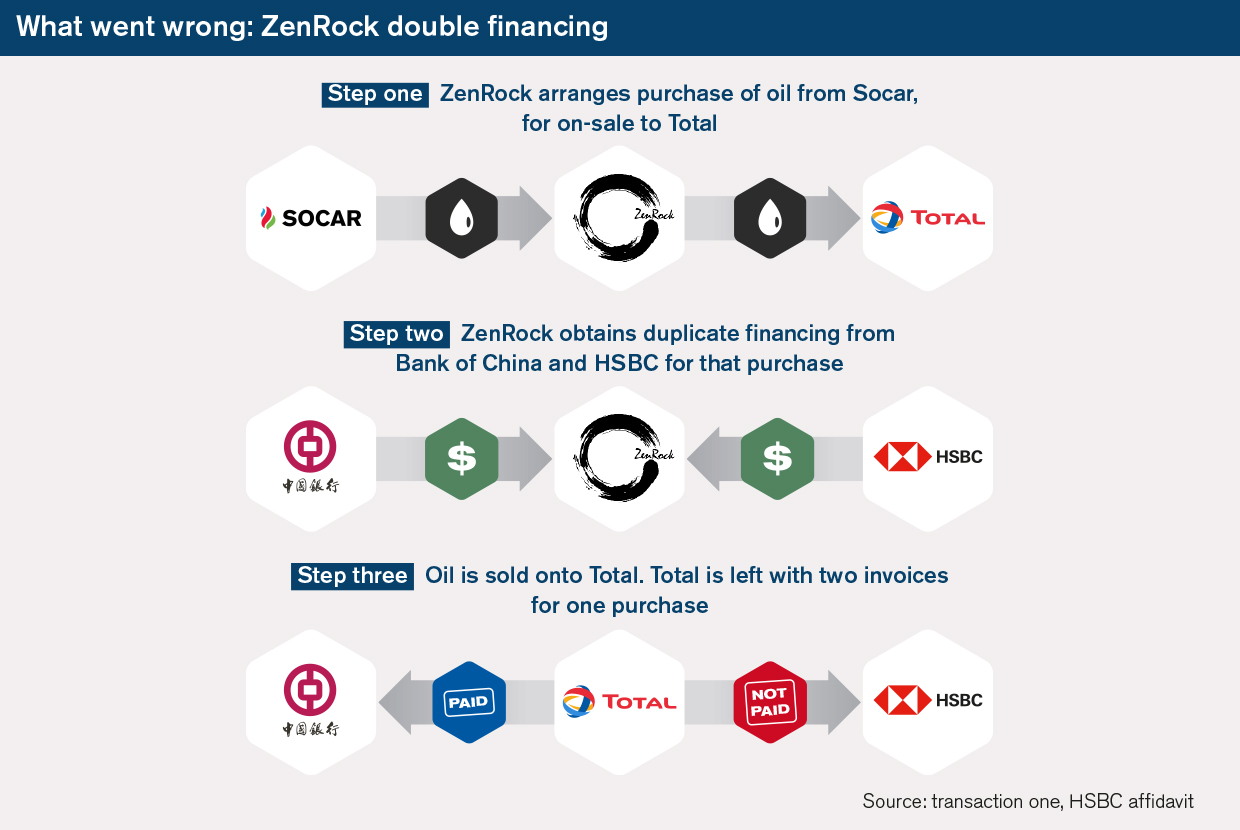

That document, seen by GTR, centres on two transactions carried out by ZenRock. The first was the use of a letter of credit to facilitate the US$35mn purchase of just over 880,000 barrels of crude oil from Azerbaijan’s Socar, to be sold on to the trading arm of French oil giant Total.

HSBC says it expected to receive repayment from Total, but when no funds arrived it discovered that another invoice for the same cargo – although with a different date – had already been paid to Bank of China. At that point, HSBC says, it “became clear that [ZenRock] had engaged in multiple financing in respect of the same cargo with more than one financial institution”.

The second transaction relates to ZenRock’s purchase of nearly 1 million barrels of Djeno crude from China-headquartered Rongsheng Petrochemical, which was again to be sold on to Total.

HSBC, at this point already concerned about ZenRock’s conduct, contacted Total. The bank was told Total had entered into an “offset agreement” with ZenRock, meaning the balance payable had fallen from US$16mn to less than US$92,000.

The bank says that agreement “came as a complete surprise” and appeared to be a breach of its contractual agreements with ZenRock. The agreement also involved Total selling ZenRock the same quantity of oil that ZenRock was selling Total, with identical delivery periods, which HSBC says “strongly indicates that the sale and purchase of oil cargo was circular”.

ZenRock continued to seek further financing in May, the affidavit adds, even at one point making a “highly irregular” profit-sharing offer, but HSBC said it was unsure the trades would be profitable or even genuine in the first place.

For Blackstone & Gold’s Bhinder, these incidents should not be viewed as unique to the fuels industry. Instead, banks should pay closer attention to financing arrangements sought by commodities trading houses across the board.

“If you look across the many defaults over the years, they cut across different commodity types and the common theme tends to be an over-concentration of liquidity in the hands of a few select trading companies,” he says.

“Once that liquidity is drawn out of the market, for micro or macro reasons, that’s where a lot of things unravel.

“Some of the trades are commercially questionable in the first place. As long as the music plays, no one is going to find out, but the problems happen when there is a break in the chain. Then, two or more banks show up with the same claim, that they haven’t been paid.”

What’s next for banks?

For banks caught between pressure from regulators to keep financing commodities trade and expectations from boardrooms to cut exposure to risk, there are steps that could be taken.

Eric Chen, investment director for trade finance at Singapore-based asset management firm EFA Group, says lenders should respond by “strengthening their due diligence, collateral monitoring and management practices so as to plug the loopholes that may have been exploited by these three commodity traders”.

Chen suggests banks consider carrying out physical site visits or spot checks, for example when providing inventory finance for oil products in a tank terminal.

Though that might not currently be possible due to Covid-19 containment measures, they could also ensure majority shareholders or management have “skin in the game” by requesting personal guarantees, such as private assets they hold. Chen adds that EFA’s “rigorous approach” to underwriting helped it steer clear of any exposure to the Hin Leong, ZenRock and Agritrade defaults.

For Bhinder, banks should “start asking the difficult questions to their borrowers”. He says lawyers investigating cases tend to probe whether trades are commercially justified, how reliable firms’ balance sheets are, and if there is any likelihood of duplicate trades.

Those questions would be better answered if raised while on-boarding new customers, rather than after wrongdoing has already emerged, the lawyer says.

“I understand the pressure of a deal scenario, they have to do that quickly, but there must be a better way of testing balance sheets and understanding trade flows,” Bhinder adds. “That doesn’t mean banks should stop carrying on financing; the world needs financing to go on. We just need to be a bit more sensible and sustainable about it. If you finance someone to the hilt by a checklist it’s not really sustainable.”

A common theme in the ZenRock affidavit is that bills of lading for the oil being traded appear to go missing. Payment is instead made upon presentation of a letter of indemnity, with the seller promising to do their “utmost [to] locate and surrender” the original shipping documents.

The source close to Hin Leong says that the paper trails in commodities fraud cases are usually “messy”. They suggest that the solution would be to “get all this data – where a cargo is, certificates to ownership, sales contracts and so on – and digitise it, to reduce the scope for fraud”.

Bhinder agrees, pointing out that there has been promising progress in digitising customs documentation– essentially helping authorities clear goods quickly – but adoption of electronic bills of lading in parallel has been sluggish.

“Between goods being loaded onto a ship in the UK and loaded off a ship in Singapore, for example, there are numerous transactions on the high seas, and that’s where the magic happens. You would need to digitise that part too,” he says.

“Why has adoption been slow? It makes you wonder whether there are vested interests in how this kind of business is conducted using paper bills.”

In the immediate term, banks active in Singapore’s commodity trading sector face a difficult decision. As of press time, Jean-François Lambert, founding partner of consultancy firm Lambert Commodities, says it is too early to say whether banks are likely to hasten de-risking.

“Clearly Singapore needs the banks and especially international banks to keep financing commodity trades, which is a key sector for the city-state,” he tells GTR. “For now they are in the middle of the storm, and it is rather difficult to pull out unless for compelling reason such as frauds.

“Banks should stand by their customers in these difficult moments – and they probably do.”