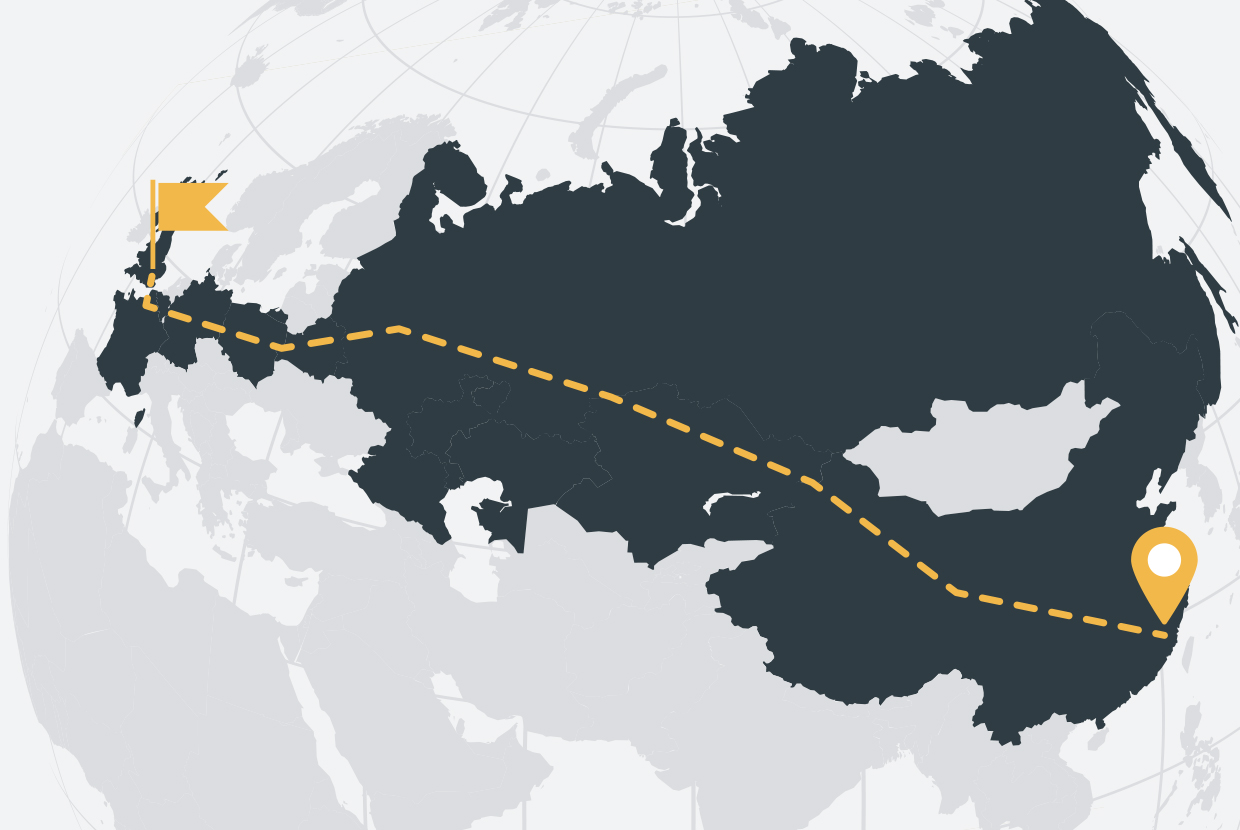

The latest phase of China’s One Belt One Road initiative saw a train depart from Yiwu province in China on New Year’s Day and pull in to Barking, London, just 18 days later. Aleya Begum reports on the new service and the lack of reception in Europe.

When the first ever freight train from China to London arrived in Barking earlier this year, it transported more than garments, bags and shoes. It also carried a grand dream of reigniting East-West trade along the old silk road routes that date back to the Han dynasty.

But, the 18-day service from Yiwu to London isn’t the first from China to Europe in recent times. In fact, the first direct train to the continent arrived in Germany back in 2012. Since then, some 39 routes connecting 16 Chinese cities with 12 cities in and along the European route have developed. While this may appear impressive, the flow of trade so far has been heavily in one direction, as European exporters are yet to embrace this new service.

According to Chinese container cargo operator OneTwoThree Logistics (OTT Logistics), in the five years up to the end of June 2016, 1,881 trains ran the China-Europe routes. Of these, only 502 were doing the leg back to China with European goods.

For logistics executive at OTT Logistics, Alex Dung, this is not surprising. “China is known as the world’s factory. A lot of foreign companies keep their management teams and research and development teams in their own countries, but build their factories or outsource the manufacturing in China due to lower labour costs and good production facilities. This is one of the main reasons there are lots of goods delivered from China,” he tells GTR.

While this may be the case, the cost of running empty containers back to China, or paying to have them parked in European hubs, brings into question the sustainability of the new routes and the justification of the billions of dollars being invested in infrastructure projects around them.

The goods at play

Trains from China mostly bring garments, bags, shoes and both low and high-value electrical items. Described as small commodities, they range from run-of-the-mill goods to more premium, high-end merchandise, such as 3D printers, ATMs and high-tech parts for factories and production lines.

Trains returning to China have typically taken back European goods including car parts, wine, olive oils, pork products, and other western luxury goods that are in high demand by a growing middle class with a desire for ‘prestigious’ European brands.

“I have a good friend who made a huge fortune as a procurement manager for western companies like Walmart, sourcing in Asia. He told me he is now sourcing [fashion garments] in Italy and the UK to sell in China because the new middle classes are looking for this,” says professor of international political economy at IMD, Jean-Pierre Lehmann. “Walking around parts of Shanghai [these days] is like walking around the Champs Elysees or South Kensington.”

China has also become one of the biggest markets for premium food products. It is among the top importers of Bordeaux wine, and an increasingly high-protein diet among the locals has pushed up the demand for prime beef and meats, adds Lehmann.

Based in Shanghai, head of trade in China at Wells Fargo, Chen Ye, confirms this demand on a personal level: “I have a three-year-old son and we try to buy him things that are manufactured in Europe, or the US, to give him the ‘best’. In China, there are millions of people like me, they think that made in UK, made in Germany goods are good for their children.

“Today, people travel to Europe and bring stuff in small quantities. Once you have convenient and low- cost transportation to import the goods from Europe, that opens a big door. There is huge demand here in China.”

According to the European Commission (EC), the EU is China’s biggest trading partner, while China is the EU’s second-largest trading partner after the US. EU-China trade has increased dramatically in recent years and China is now the EU’s biggest source of imports as well as one of the EU’s fastest-growing export markets. The EU has also become China’s biggest source of imports, and trade between the two currently stands at over €1bn a day. So if the demand is there, why are more than two thirds of the trains going back empty?

Competition and logistical challenges

The new freight trains have been marketed as faster than shipping and cheaper than air. According to OTT Logistics, the cost of rail freight is half that of air, and transport times are twice as fast as the 30-odd days by sea. While market observers expect the trains to put some pressure on air cargo, the limited capacity of the trains (which can take 30 to 50 containers) compared to that of ship carriers (which can carry as many as 11,000) is unlikely to make it a major competitor for shipping just yet.

Shipping companies that GTR spoke to say that while they are “following the initiative closely” they do not see the trains as an alternative to ships.

“We believe the One Belt One Road (OBOR) correctly identifies connectivity as a significant enabler of trade. Bringing together China and Southeast Asia, South Asia and the Indian Ocean through rail and road links is no doubt of big value and importance on developing trade and bringing down costs,” says communications officer at Maersk Transport and Logistics, Michael Christian.

“As to transporting containers over land via rail from China to Europe and the Middle East, this is also interesting. However, the volumes moved by sea between China or Asia and the Middle East or Europe are enormous, which is why we see a land option more as an additional route rather than an alternative to the sea route.”

Although this carries true today, stops along the Silk Road route are on course to potentially changing this. At the Khorgos Gateway, on the borders of China and Kazakhstan, the railway container port currently has capacity to process 540,000 twenty-foot equivalent units (TEU) annually, with six berths where multiple trains can be handled at the same time. Within five years, its management predicts this to be over 1 million TEU – which is more than many seaports.

As well as capacity constraints, the huge overland distances the trains cover also give rise to various other challenges. The railway lines not only require vast continuous maintenance along the 12,000km stretch to Europe, but the tracks themselves are different between regions. Railway lines in Kazakhstan, Russia and Belarus use wider gauges, while China and Europe use a standard size. This means that cargo has to be transferred from one train to another every time it crosses between two regions, which will happen at least twice in each direction on the China-Eurasia-Europe route. This not only increases travel time but also customs and security risks.

“It’s just the type of thing that complicates matters,” says partner at King and Spalding’s international trade practice, Iain MacVay. “An airplane takes off and lands and there are no customs. The same with a ship. A train [moving over land] – there might be little bit more risk there.”

Train operators have also been struggling with setting regular timetables and maintaining set schedules. A reluctance to run trains without sufficient cargo and a preference for waiting for full loads means not being able to offer businesses guaranteed delivery times. Without a delivery commitment, companies are naturally reluctant to book cargo. Some of the routes from Germany and Spain now have regular weekly departures, and are subsequently enjoying better order books. Operators are working on offering this across the board and are optimistic that it will lead to more bookings.

Manager of OTT Logistics in London, Oscar Lin, tells GTR that the London-China train is still waiting to fill up: “At the moment we are taking orders and bookings. There is no schedule, it depends on business. In future, if business is big enough, we will consider scheduling a regular train.”

Ideological disparities

One could argue that many of the issues listed are all teething problems that any new service is likely to encounter. So perhaps the most critical issue isn’t technical, or commercial, but in fact ideological.

While China has gone to extreme lengths to promote its OBOR initiative, it has received mixed reactions from other countries and the lack of narrative from Europe is telling of a dream not (yet) shared.

China first mooted its ambitious OBOR initiative in 2013. Consisting of a land and a maritime branch, China says OBOR is a development strategy and framework that will boost connectivity and co-operation between it and the rest of Eurasia by encompassing around 60 countries through a network of port, rail, road and pipeline infrastructure.

China argues that OBOR will enhance interconnectivity in a geographic area stretching from Far East Asia through Central Asia, the Middle East and Russia to Europe, which generates around 40% of global GDP, represents about 70% of the global population and has an estimated 75% of known energy reserves. The Chinese government estimates projects will take 30 to 35 years to complete and require significant funding, but aspires to achieve annual trade worth US$2.5tn between the countries located along OBOR within 10 years.

For its part, China started with an investment commitment of US$40bn for OBOR and created two international banks to fund projects: the Asian Infrastructure Investment Bank (AIIB), which now has 82 countries participating, including several European countries; and the Brics’ New Development Bank in co-operation with Russia, Brazil, India and South Africa. Chinese spend so far is quoted close to US$1tn, with China saying it expects to spend a cumulative US$4tn.

However, the grand scheme hasn’t convinced everyone. While a move to enhance connectivity and fill the huge infrastructure gaps across Asia has been welcomed and drawn considerable financial interest, there are concerns regarding China’s hegemonic ambitions.

“Many of the train lines are connecting to important ports in Europe, which makes the international trade routes more connected. But the concern is that China could one day use those lines and connections for political or military purposes,” says Ye at Wells Fargo. “The Chinese government needs to be careful and address those concerns.”

Intra-regional relationships and rivalries between other countries also come into play. While countries like Kazakhstan, Mongolia, Turkmenistan and Uzbekistan welcome the new routes that allow these previously marginal markets to potentially become more significant hubs, such developments raise concerns for Russia.

“Even though [Russia and China] share a huge border it’s not a particularly cuddly relationship – it’s one of mutual suspicion which has existed over centuries,” says Lehmann at IMD. “The Russians see Central Asia as their backyard. Now many of these countries do more business with China than with Russia so there’s a sense of ambiguity there with the Russians.”

Likewise, China’s relationship with India has been generally tense, so the China-Pakistan corridor that has now emerged makes the Indians very nervous, he adds.

Lack of European narrative

In Europe, there has been limited, even dismissive discourse on OBOR. In a roadmap document titled Elements for a New EU Strategy on China, published last June, the EC mentions OBOR briefly over a few paragraphs. It outlines the aim of creating “synergies” between China’s OBOR initiative and its own policies and projects on the basis that China “adheres to market rules and international norms”.

However, analysts have pointed out that the initiative is more than transport and infrastructure, and its success should not be measured by a quantitative index of connectivity or speed. They argue that OBOR is attempting to “change the rules organising the global economy” by allowing China to reorder global value chains.

“The trains from China to Europe should be seen in the overall context of what is the global Chinese strategy for the 21st century. To look at the trains from a cost benefit analysis in the short term doesn’t really give much satisfaction,” says Lehmann.

“The Chinese assemble imports bought in from other countries, like Japan, Korea, Germany and then export them. Only 6% of the value is made in China. This has been the pattern from around the mid-1980s. China now has the desire to go up the value chain, and its global strategy is to provide a framework for its high exports but also for its capital so that it can consolidate the supply chain in the broad sense of the term.”

For Bruno Maçães, partner at Flint Global, who was a former non-resident associate at Carnegie and former EU secretary for the Portuguese government, the argument goes further. In his November 2016 paper, written for Carnegie, China’s Belt and Road: Destination Europe, he argues that Europe needs to confront the losses it may incur when Chinese companies start to be better represented in high-value segments of important value chains, but also questions what set of rules will govern the way these chains are organised.

He highlights that for China, industrial policy, development and innovation is a process that is as much as possible organised at the political level, and most large Chinese multinationals are not only state-owned but effectively managed through goals and strategies defined in political channels: a model and approach that few, if any, European businesses or policymakers believe in.

He concludes that OBOR is above all a challenge to Europe – a challenge to which Europeans have yet to respond to.