Trade with Iran has become close to impossible since the collapse of its 2015 nuclear deal with the EU and US. However, suspicious activity in nearby shipping channels suggests that outlawed transactions are still happening. How can financial institutions minimise their risk of exposure to sanctioned exports, and are there still opportunities for legitimate trade with the embattled Middle Eastern state? John Basquill reports.

July 14, 2015 was a landmark date in the long-running feud between Europe, the US and Iran. Iranian officials agreed to terminate the country’s nuclear programme, and in exchange, would benefit from the removal of crippling sanctions – including on petroleum exports.

Trade with the EU soared. Over the following three years, the total value of the bloc’s goods exports from Iran increased almost eightfold, from €1.25bn in 2015 to €9.45bn in 2018, according to European Commission figures.

But that momentum stalled in May 2018, when US President Donald Trump announced the US would withdraw from the agreement, officially termed the Joint Comprehensive Plan of Action (JCPOA).

Though the EU remained keen to keep the JCPOA alive, tensions continued to escalate between the US and Iran, and after Qasem Soleimani – commander of Iran’s elite Quds Force – was killed in a US air strike in January 2020, Iran’s government formally announced it too was abandoning the deal.

Because of the US’ fearsome secondary sanctions regime – which means non-US companies carrying out non-US activity can still be the subject of enforcement action – the end of the JCPOA made legitimate trade with Iran near impossible, aside from the provision of humanitarian aid such as medical supplies.

However, there are signs that the country’s potentially lucrative petroleum export industry has continued to stay active – meaning oil traders, banks and insurers could be at risk of unwittingly supporting sanctioned trade.

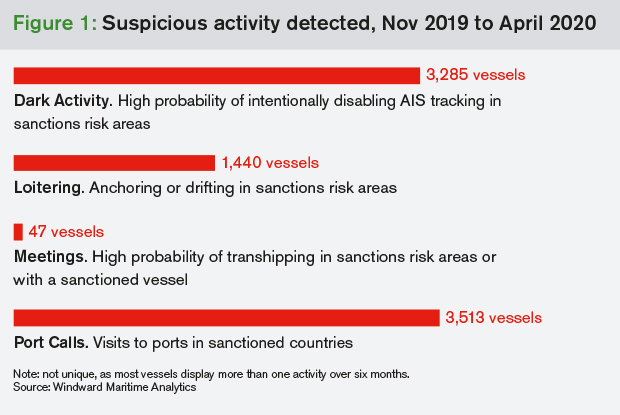

Suspicious vessels

Windward Maritime Analytics, a Tel Aviv-headquartered firm that carries out tracking and behavioural analysis on potentially suspicious ships, warns in a February report that it is becoming “increasingly difficult for companies operating in the maritime ecosystem to know which vessels are safe to do business with”.

In the six months prior to April 2020, Windward says 1,280 unique vessels exhibited suspicious behaviour in the waters around Iran – far higher than the equivalent figure for Russia, Venezuela or North Korea, which are also subject to US-imposed restrictions on trade. Of those, 496 were tankers and 784 were cargo ships.

Specific examples cited include two general cargo ships under the flags of Russia and Panama that were spotted “loitering” close to Iran, a port call from a Russian-flagged oil or chemicals tanker, and a port call from a Togo-flagged cargo ship. Port calls were the most common suspicious activity detected, with more than 3,500 taking place between November 2019 and April 2020.

Another sign of potentially illicit behaviour is vessels switching off their automatic identification system (AIS) transponders. Though initially developed to prevent collisions, AIS signals are now used to monitor ships’ whereabouts, and must remain switched on at all times.

In a case study of potential sanctions evasion linked to Iran provided to GTR, Windward says that in May 2019, 19 crude oil tankers – 3% of all crude tankers operating in the Gulf – switched off their AIS and “went dark” while operating in the area.

Between May and June, those 11 tankers made 68 ship-to-ship meetings in UAE waters, which included the transfer of cargo to other tankers.

That does not necessarily point to illicit activity – ship-to-ship transfers are not prohibited and AIS signals can easily be lost, particularly in crowded seas – but it is not always straightforward to identify which ships are conducting legitimate trade and which are not.

“While eight of those [19 tankers] were Iranian flagged and obviously a no-go for trade, the other 11 aren’t as easy to screen: seven were Panamanian, two Liberian and two Vietnamese,” Windward says. “None of them is registered by an Iranian company or made port calls in Iran, making them almost impossible to detect using existing vessel tracking and list-based screening.”

Sometimes, illicit activity only becomes apparent after the event.

One of those 19 vessels was the notorious Grace 1, which at that time was picking up cargo offshore then transporting it to Singapore. But shortly afterwards, Grace 1 found itself at the centre of a diplomatic row between the UK and Iran.

The ship was seized by British Royal Marines in July 2019 amid claims it was transporting 2.1 million barrels of Iranian crude oil to Syria. Foreign secretary Dominic Raab described the alleged sale as “part of a pattern of behaviour by the government of Iran designed to disrupt regional security”.

Though released after Iran’s government promised the ship’s load would not be delivered to Syria, Windward’s report says that prior to that incident its ties to the country would have been difficult to detect.

“Investigating its ownership would lead nowhere. According to Equasis, it is owned and managed by Singaporean companies, and its real, beneficial owner remains unknown, passing screening against databases of sanctioned entities (such as SDN lists) and rules relating to the country of registration,” it says.

“Going beyond ownership to investigate the vessel’s port calls and historical locations would also lead to a dead end. The Grace 1 was last detected in port almost two years ago, in Qingdao, China. Since then, it’s been operating continuously at sea; any port calls it may have made have been masked by turning off its mandatory AIS transmissions.”

For Windward, traders and banks can limit their potential exposure to illicit shipping activity by adding behavioural analysis to existing due diligence checks. In the case of Grace 1, it says “signs were there for at least six months”, including a 10-day period when the ship went dark near Bushehr, a port city in south-west Iran.

According to Ron Crean, Windward’s vice-president for commercial business, that shift towards behavioural analysis of ships’ movements is already being noted by regulatory authorities, including the US’ fearsome sanctions regulator, the Office of Foreign Assets Control (OFAC).

“We expect OFAC’s focus to become much more focused on ships’ behaviour, which is the hardest and most opaque element of this pattern analysis,” Crean tells GTR.

“You may be exposed as a company if you’re doing business with a vessel even if it’s not on a sanctions list. Additional checks for sanctioned activities based on vessel behaviour are now a minimum requirement.”

Sanctions enforcement

OFAC, which is housed within the US’ Department of the Treasury, has been highly active in tightening controls against Iran in recent months.

In March, several companies and individuals were added to its list of entities with whom trade is prohibited, having been accused of facilitating the sale of Iranian oil to the Syrian regime. The department said supplies had been smuggled through the port of Umm Qasr in Iraq, with the illicit payments routed through Iraqi front companies.

Five companies in the UAE were also sanctioned earlier in the month, again for allegedly handling sales of Iranian petroleum and petrochemicals. The department said that throughout 2019, these companies “collectively purchased hundreds of thousands of metric tons of petroleum products from the National Iranian Oil Company”.

“Iran’s petroleum and petrochemical industries are major sources of revenue for the Iranian regime, which has used these funds to support the Islamic Revolutionary Guard Corps-Quds Force’s malign activities throughout the Middle East, including the support of terrorist groups,” it said, adding that at least three of the UAE companies “falsified documents to conceal the Iranian origin of these shipments”.

The companies were named as Petro Grand FZE, Alphabet International DMCC, Swissol Trade DMCC, Alam Althrwa General Trading LLC, and Alwaneo LLC.

Other companies accused by the US government of facilitating Iranian oil sales include Triliance and Sage Energy, both based in Hong Kong, as well as China-based Peakview and UAE-based Beneathco. The latter firm was accused of “hiding the origin of Iranian products destined for the United Arab Emirates”.

None have a prominent internet presence or could be reached for comment.

If banks have facilitated trade transactions on behalf of sanctioned entities, the most obvious risk they face is enforcement action. In the case of the US alone, OFAC has issued fines totalling nearly US$1.3bn from the start of 2019 until April 2020 for sanctions-related offences.

The two largest individual penalties in that period were both issued to international banks accused of facilitating transactions linked to Iran’s petrochemicals trade – albeit prior to the JCPOA. Standard Chartered was fined US$639mn by OFAC in April 2019, part of a US$1.1bn settlement with US authorities, and a few days later, UniCredit was issued with a US$611mn penalty as part of a US$1.3bn settlement.

Now, following the collapse of the JCPOA and the reinstatement of secondary sanctions, Washington, DC-based Brian Fleming – a lawyer at Miller & Chevalier and a former counsel within the US Department of Justice – says banks are understandably “fearful of the consequences” of doing business in the country.

“We have advised many, many companies, including financial institutions on this issue,” he tells GTR. “There were a number of banks that had gone back into Iran, or were considering doing so, when all of a sudden the US started threatening all kinds of consequences against those doing business in the country – especially business related to petroleum and petroleum products.”

But for Fleming, the risk goes beyond financial penalties for wrongdoing. He points out that banks continuing to attempt to support trade with Iran could earn an unwanted reputation.

“Even if a bank might be doing business it believes is permitted under the US secondary sanctions regime, many are concerned they may make a mistake, or that their banking and commercial partners may view them as being too risky a counterparty. That means the vast majority have chosen to unwind whatever business they had there,” he says.

“In a sense, that’s how the sanctions are intended to work: to deter non-US parties, especially in the financial sector, from working with Iran, because they’re either fearful of the direct repercussions from the US government or recognise that it’s nearly impossible to do that business in any kind of cost-effective way.”

Humanitarian trade and Covid-19

There are exceptions to the US’ sanctions regime against Iran. The provision of humanitarian aid, such as pharmaceuticals or medical supplies, can be allowed in some cases, as can certain agricultural products and personal remittances.

Since the outbreak of Covid-19, US officials have been at pains to emphasise that such trade is still allowed. Alongside the government’s March announcements that several companies had been added to its list of sanctioned entities, Treasury secretary Steven Mnuchin insisted that “the Trump administration… remains committed to facilitating humanitarian trade and assistance in support of the Iranian people”.

He added that the regime “maintains broad exceptions and authorisations for humanitarian aid, including agriculture commodities, food, medicine, and medical devices to help the people of Iran combat the coronavirus”.

Iran was one of the first countries to suffer a widespread outbreak of Covid-19 after China, with several high-profile figures – including the government’s deputy health minister, Iraj Harirchi – contracting the virus weeks before it became widespread throughout Europe and the US.

As of April 30, more than 6,000 people in Iran have died after testing positive for the virus. The severity of the outbreak in the country has accelerated calls to ease the provision of medical aid, including pleas from humanitarian pressure groups to lift sanctions completely for a limited period.

Though the US government has shown little appetite to withdraw sanction completely, it has started facilitating shipments of medical supplies.

Notably, the Department of the Treasury announced in February that the Swiss Humanitarian Trade Agreement (SHTA) is fully operational, providing a government-backed channel for sending shipments of food and medical supplies to Iran. Pilot operations at the start of the year facilitated a shipment of medicines valued at around US$2.5mn.

John E Smith, a partner at Morrison Foerster in Washington, DC and a former OFAC director, told GTR at the time that SHTA “might provide a safer or risk-free alternative for companies and governments that want to send those goods to Iran”.

And in Europe, Instex – a special purpose trade vehicle set up by France, Germany and the UK specifically to bypass US sanctions on Iran – successfully completed its first transaction in March.

Instex, which works by offsetting transactions so that money does not have to be sent across international borders, facilitated the shipment of medical goods from Europe to Iran. The companies involved have not been named, but GTR understands the value of the transaction was around £500,000.

However, gaining widespread support from the banking community remains a distant prospect. For Smith, Instex remains a “test case” rather than a proven safe haven for banks and traders. “It remains unclear whether it will be a system that can become operational in a significant way,” he says.

In the longer term, trade experts suggest that a new deal with Iran may be the only way of giving sufficient comfort to the trade finance sector.

The Trump administration appears to have little interest in reviving the JCPOA, but Anahita Thoms, a partner at Baker McKenzie and of its International Trade Practice in Germany, suggests a lesson could be learned from the North American Free Trade Agreement (NAFTA).

Trump announced upon taking office in 2017 that he intended to withdraw the US from NAFTA, a 1994 free trade agreement with Canada and Mexico that came into force in 1994, describing it as a “nightmare” for the US economy.

Despite that, an agreement has been reached relatively swiftly on a new US-Mexico-Canada agreement, or USMCA, that is due to take effect in July 2020.

For Thoms, it is likely Trump sees the Iran nuclear deal as too closely tied to the legacy of his predecessor, Barack Obama, but that seeking a fresh agreement could be a way forward.

“Personally, I think it would be best to try and negotiate a new deal now, and basically start all over again,” she tells GTR.

“What is clear is Trump will never accept the JCPOA, in no small part, partly also because it’s an Obama deal. What he did with NAFTA may give us some hints as to what he’s looking for here: he wants to be the one to do the deal, and on his own terms.”