After years of growth and optimism, clouds are starting to gather over the sustainable finance market. Authorities across Europe are increasingly questioning the integrity of what is still a developing product, and with greenwashing concerns looming large over the banking sector, John Basquill examines how lenders can support sustainability without falling foul of the law.

The sustainable finance market hit record heights in 2022.

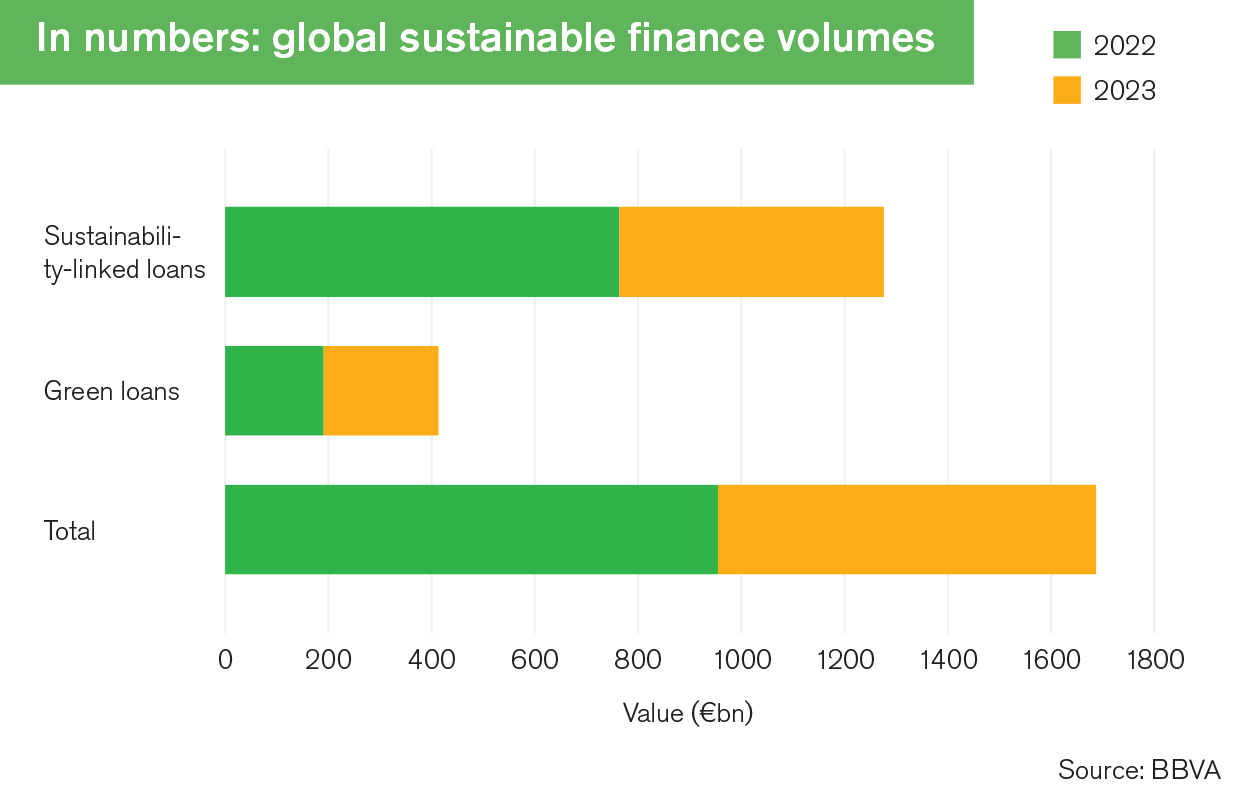

Sustainability-linked loans, where borrowers are incentivised to meet pre-agreed targets or KPIs, totalled an estimated €761bn globally, according to BBVA research.

Green loans, where funds are provided in support of environmentally friendly projects or corporate activities, totalled a further €193bn.

But last year, the market shrank for the first time. The combined total value of sustainability-linked and green loans dropped by more than a quarter, from €954bn to €731bn, the Madrid-headquartered lender estimates.

BBVA says much of that drop can be attributed to a broader decline in corporate loan volumes globally, while consultancy firm Baringa notes that the end of low-interest rate borrowing also likely contributed to the decline.

However, there is another factor. Baringa’s analysis cites “increasing scrutiny of sustainability claims”, as authorities express growing concern that such loans – although not regulated at the product level – are not working as they should be.

Misaligned incentives

In June last year, the UK’s Financial Conduct Authority (FCA) sent ripples throughout the sustainable finance sector. It warned in an open letter to bank CEOs that it had “market integrity concerns”, fearing a loss of trust could hold back wider adoption of sustainability-linked loans.

Having grilled various stakeholders in a review of the market, the authority questioned whether banks and their customers are sufficiently incentivised to incorporate strong sustainability targets into lending facilities.

In some cases, misaligned incentives are cost related. For instance, with loans where borrowers can make savings on margins if they hit sustainability targets, the FCA letter said those benefits “may be outweighed by costs and negotiation time with lenders or legal advisers”.

Alternatively, banks may feel wary of including tough penalties in situations where targets are missed, for fear of damaging client relationships. Missed targets could also cause reputational damage if made public.

The FCA letter noted that step-ups in margins do not appear to have increased significantly despite steep rises in interest rates. For investment-grade borrowers, steps-up appear to be capped at around 0.05%, it said, while for lower-rated and leveraged loans, typical figures are around 0.25-0.3%.

The authority added that conflicts of interest could occur within banks if staff remuneration is linked to hitting sustainability targets, as that could encourage lenders to accept weaker KPIs from borrowers.

Among Europe’s 25 largest banks, the most common climate-related KPI for executive bonuses is hitting green and sustainable finance targets, according to a 2022 assessment by responsible investment charity ShareAction.

Though the FCA said it had no plans to introduce regulatory standards or a code of conduct specific to sustainability-linked lending, it would “reconsider this if the market needs it”, noting market participants were keen to reduce the threat of greenwashing accusations.

The regulator is also introducing an anti-greenwashing rule from May 31 this year that will require all regulated firms to ensure sustainability claims are clear, fair and not misleading.

The FCA is not an outlier on the subject. Its letter came hot on the heels of an announcement by the European Banking Authority (EBA) that it was considering recommending EU-wide regulatory changes that would directly address greenwashing by financial institutions.

The authority said it had seen “a clear increase in the total number of potential cases of greenwashing across all sectors, including for EU banks”. Earlier EBA data showed nearly a fifth of greenwashing allegations worldwide were in the financial sector, with more than 200 such cases reported in the EU alone in 2022 – up from just 40 in 2018.

The most common allegations cited against EU lenders related to business strategy, such as misleading the public into believing a bank is fighting climate change “while investing in a company allegedly linked to deforestation in the Amazon” or “provid[ing] financing to oil companies operating in the Arctic”.

The EBA also singled out sustainability-linked loans with “weak structures or contractual commitments”, for instance where a borrower faces no penalty for missing targets, as an area in need of scrutiny.

Regulatory intervention

The regulatory environment around sustainable lending – or more accurately, the lack of it – has proven to be a mixed blessing for its uptake.

“On the one hand, that’s good because it allows flexibility for innovation, and we’ve seen rapid growth,” says Greg Brown, a partner at Allen & Overy and head of the firm’s finance and impact investment group.

“But because it’s fundamentally unregulated, it relies on the choices and behaviours made by market participants themselves,” he tells GTR. “Now there is more sense of danger around misaligned incentives, what we’re seeing is a bit of retrenchment.”

That retrenchment could be felt more keenly in trade finance, as much of the initial growth of sustainability-linked and green financing was concentrated among blue-chip borrowers.

Niamh Dennehy-Maher, counsel at Allen & Overy and a trade and commodity finance (TCF) specialist, says sustainability-linked provisions “were already becoming almost a standard feature of loans in the investment-grade and corporate lending markets”.

“Loans in the trade and commodity finance market are certainly going in a similar direction – which is not surprising, given the clear case for green and sustainable lending in the TCF space, for example in the case of agricultural commodities. But in terms of how developed that market is, it’s still catching up with the investment-grade and corporate lending space,” she tells GTR.

For institutions keen to increase sustainable finance provisions, the Loan Market Association’s (LMA) Sustainability-Linked Loan Principles are a useful resource.

Initially published in 2019 and revised two years later, the principles already address some of the issues pinpointed by last year’s FCA letter – including those related to concerns over greenwashing.

Andrew Stanfield, counsel in Linklaters’ banking team, points out that according to the LMA principles targets “must be beyond business as usual and cannot be less ambitious than other targets announced publicly”.

“The principles are aimed at ensuring these loans have credibility and integrity,” he tells GTR.

Although voluntary, the association’s guidance is supported by the FCA. The authority’s letter noted that revisions made to the principles in recent years address some of the issues it identified, adding: “There has been a positive reaction to these from the market and we believe a broader adoption of the existing [principles] would drive further growth.”

But are regulators likely to go further, addressing misaligned incentives by intervening directly on the product side?

“One problem with regulators creating incentives is that in the corporate lending market, you tend to have large banks and large borrowers who are capable of making their own choices, and it’s already a mature product,” says Brown of Allen & Overy. “It could be a retrograde step to try and regulate one part of it while leaving the rest as it is.”

Avoiding greenwashing

More likely, Brown says, is that regulators tackle the effects of an unregulated market – predominantly, the risk of greenwashing – by increasing scrutiny of the claims made by banks about their sustainability-linked and green loan activity.

“They will probably care about what a bank is saying to its shareholders, stakeholders and the public at large, and at some point, might feel the need for some overall framework that does more than the LMA principles,” he says. “Otherwise, you are relying on good intentions and end up with a lack of consistency.”

But tackling greenwashing is complicated, not least because it is not always deliberate.

Simon Thompson, chief executive of the Chartered Banking Institute and chair of the Green Finance Education Charter, suggests that regulatory initiatives “will help root out instances of deliberate greenwashing, but I am afraid this is only the tip of a rapidly melting iceberg”.

“Inadvertent greenwashing should be of much greater concern. In my view, this is a much greater threat to the integrity of sustainable finance.”

Examples of inadvertent greenwashing include highlighting the benefits of a facility without considering associated negative effects, such as harm to local communities, or sincerely describing products as sustainable but without sufficient independent measurement or verification.

Tackling those kinds of issues requires access to reliable and detailed information on the impact of a borrower’s activities. Though larger corporates are more likely to have detailed sustainability strategies in place, mitigating those risks poses more of a challenge to smaller and mid-sized companies.

“That really matters, because to avoid greenwashing it’s critical to get those details right. For that, data is absolutely critical,” says Linklaters’ Stanfield.

“Say you have two differently sized companies, both with targets linked to absolute CO2 emissions. Clearly, the target for one will not be suitable for the other, so to set the targets and KPIs appropriately, you need to have sufficient data. The data is key to driving credibility of the product.”

A representative from a major European bank, speaking under the Chatham House rule at an industry event in early 2024, gave a real-world example of two clients with the same activities in the same geographies.

One reported 80% alignment with targets set under the EU taxonomy for sustainable activities, and the other was reporting 0%, they said.

“We need our clients’ data in terms of alignment with the taxonomy,” they said. “But we’ve got to deal with the fact this data is not audited yet, which makes it complex for us.”

What can the market do?

An analysis of greenwashing risks in the trade and commodity finance sector, published by law firm HFW in November, urges lenders and borrowers to “exercise caution” when arranging sustainability-linked facilities, so as to avoid accusations of greenwashing.

“In short, sustainability targets embedded in these products should be selected extremely carefully to ensure that they are material, robust and meaningful,” it says.

One risk to borrowers is that their lender declassifies a sustainability-linked facility if targets are not met. That borrower may then be prohibited from referring to the sustainability linkage in future public statements, posing the risk of reputational damage.

“Discussions and cooperation with banks in the sector are an integral part of the process,” HFW’s analysis says. “However, trade finance professionals should take care not to rely on a financier’s own sustainability frameworks when making sustainability or green assertions about a trade finance product or underlying goods.”

Allen & Overy’s Dennehy-Maher adds the LMA principles state that targets “need to be set at the outset of the loan, not left as something to be thought about later”.

“It’s easy to refer to sustainability in a term sheet but a sustainability label without anything meaningful behind it is clearly not right,” she says.

On the data side, the International Chamber of Commerce (ICC) is seeking to tackle the issue by applying a graded scale to individual transactions, producing an overall sustainability score based on five components – the seller, buyer, transportation, purpose and goods themselves.

An initial pilot of the scheme, Wave 1, was launched last year in the textiles sector. The ICC announced in December that Wave 2 would expand the scope to the energy and automotive industries, and provide a more granular grading system.

Responding to industry feedback on the pilot, Wave 2 specifically sought to address concerns from corporates that they lacked adequate financial incentives to seek sustainable financing facilities, and that sharing data with lenders is “time-consuming and labour-intensive”.

Ultimately, the ICC hopes that standardising and automating “large elements of the framework” will resolve those issues, making facilities both cheaper and more widely available.

Speaking on the sidelines of February’s GTR Mena event in Dubai, ICC secretary general John Denton said: “The idea is then to provide a certification process, which gives an improved prospect for lowering the cost of financing, and improving the ability to participate in global value chains.”

But in the immediate term, the signal from Europe’s regulators is clear: sustainability claims are being watched more closely than ever.