As Africa’s leaders look to secure the continent’s recovery from the Covid-19 pandemic in the face of numerous headwinds, Eleanor Wragg outlines the outlook for trade and explores some of the key challenges the region must tackle.

The most recent economic outlook from the International Monetary Fund (IMF) paints a gloomy picture for Africa. Previously the world’s second fastest-growing region, trailing only developing Asia, the events of 2020 plunged the continent into a recession for the first time in a quarter of a century. Although global growth is set to reach 6% in 2021, Africa’s recovery will be far more muted, at just 3.4%, putting it at the bottom of the world’s regions in terms of economic expansion this year.

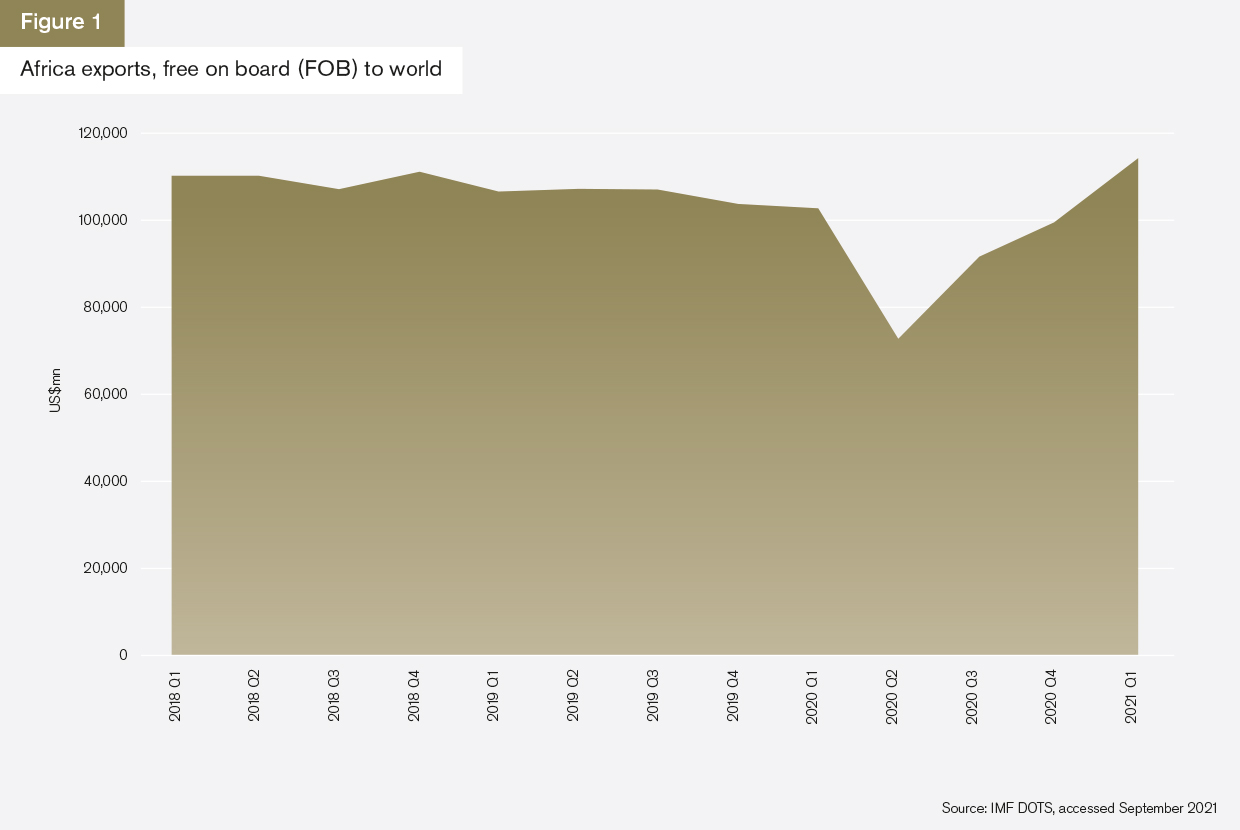

However, Africa’s trade recovery is now underway (see figure 1), with the IMF’s Direction of Trade Statistics (DOTS) showing that, after a sharp dip during the worst of the pandemic, exports reached US$113.2bn in the first quarter of 2021, topping pre-Covid levels.

A pariah continent

However, one quarter of stellar figures does not a recovery make. The near-term prospects for African trade depend critically upon the path of the pandemic. While talk in other global regions revolves around the reopening of economies and the resumption of activities, Africa is continuing to see an increase in both Covid-19 fatalities and cases, according to the Africa Centres for Disease Control and Prevention, a public health agency of the African Union (AU). Several countries, among them South Africa, Gabon, Botswana and Namibia, are classified by the agency as undergoing “a very widespread or fast-growing outbreak”.

This is largely due to the region’s comparatively slower vaccine rollout, where most countries are unlikely to see broad coverage – defined as at least 60% vaccination – before the end of 2023.

September data from the World Health Organization (WHO) shows that 42 out of Africa’s 54 countries – or nearly 80% – will fail to meet the global target of vaccinating the most vulnerable 10% of every country’s population by the end of that month, set by the World Health Assembly, if the current rate of vaccine deliveries and inoculations continues.

“Vaccine hoarding has held Africa back and we urgently need more vaccines, but as more doses arrive, African countries must zero in and drive forward precise plans to rapidly vaccinate the millions of people that still face a grave threat from Covid-19,” says Matshidiso Moeti, WHO regional director for Africa.

“We are not getting vaccinated at the rate that we need to in Africa, and we’ve got less than 3% of the world’s vaccines. Unless we sort that out, we’re going to be a pariah continent locked out of the global recovery because we are banned from travel, the borders are closed, and we are still in lockdown,” Ronak Gopaldas, director of South African-based risk management firm Signal Risk, tells GTR.

However, there is some cause for optimism. In August this year, almost 21 million vaccine doses arrived in the region via the COVAX facility, a greater number than those delivered in the previous four months put together. Meanwhile, the AU’s African Vaccine Acquisition Trust (AVAT) has begun monthly deliveries of the Johnson & Johnson single-shot vaccine, marking the first time AU member states have collectively purchased vaccines.

“The vaccines, partly manufactured in South Africa, are a true testament that local production and pooled procurement as envisioned in the African Continental Free Trade Area (AfCFTA) are key to the attainment of a more sustainable post-Covid economic recovery across the continent,” says Vera Songwe, United Nations under-secretary general and executive secretary of the United Nations Economic Commission for Africa, adding that Africa can create over 5 million more jobs if additional health commodities are manufactured on the continent.

Moving downstream

The fact that the AVAT initiative’s vaccines are being produced at the Aspen Pharmacare facility in Gqeberha in South Africa is not only a success for the vaccine roll-out, but also forms part of a wider trend of regionalisation that has been driven by Covid-19.

The early days of the pandemic saw manufacturers in many markets re-purpose their production capacity to supply essential goods for the public health response, including personal protective equipment. But, as a growing number of traders experienced input shortages that threatened their operational capacity, making a wider range of goods closer to home began to make sense.

“Companies have adjusted to the limited access to global supply chains, and have invested in local manufacturing and processing capabilities to move further downstream,” Rob Withagen, co-founder and CEO of Asoko Insight, a corporate data platform for Africa, tells GTR. “This was first of all driven by necessity during Covid, but now some of these companies have had an eye-opening moment where they see that they can actually secure their supply chains, be much less dependent on what is happening in Asian countries, and also make a profit.”

According to Withagen, the industries where this trend is most visible include, unsurprisingly, the pharmaceutical space, but also the wider fast moving consumer goods (FMCG) sector. “Although a lot of the evidence is anecdotal at this point and it is too early to talk about numbers, there are several examples of companies across anything from beverages to food and toiletries that used to have a purely trading focus and are now setting up manufacturing, processing or assembly operations, just to step into the gaps in supply chains.”

This marks a step-change for the region, which, due to its abundance in natural resources, has largely focused on the supply of upstream intermediate inputs rather than downstream finished goods.

Rising wages in China have also created opportunities for low-cost, labour-intensive manufacturing activities in Africa.

However, as the IMF states in its most recent regional economic outlook, it remains to be seen whether Africa’s exporters can consolidate their move downstream. “Import substitution industrialisation has often failed in Sub-Saharan Africa, as high tariffs and subsidies aimed at protecting a local monopoly have also tended to encourage state capture and corruption,” the IMF says.

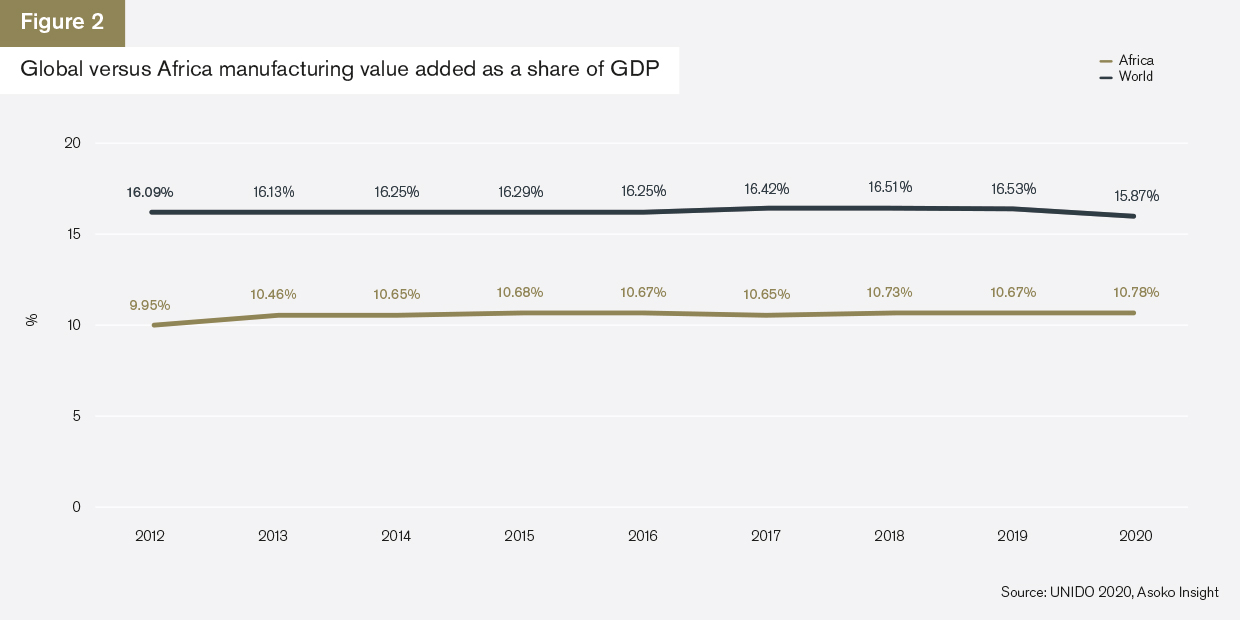

What is clear, however, is that a move towards greater manufacturing capacity in Africa was already underway prior to 2020. Comparative data from United Nations Industrial Development Organisation (UNIDO) and compiled by Asoko Insight covering the period from 2012 to 2019 shows that Africa’s share of manufacturing value added (MVA) in GDP has been increasing faster than the world average, growing annually by 6% compared to a global rate of 3%, albeit from a lower baseline (see figure 2).

Mind the gap

Finding the finance for any new manufacturing trade flows will likely be a challenge, however.

A recent report by the African Export Import Bank on the impact of Covid-19 on trade finance highlights that a lack of liquidity and increased risk aversion have made it harder for exporters to get the funds they need, and that this trend shows little signs of abating.

Published this year, the report, which draws on data from banks and financial institutions accounting for around 58% of total Africa banking assets, covers the first four months of 2020, and finds that letter of credit business and correspondent banking operations witnessed a “significant slump”, while 30% of respondents indicated an increase in trade finance rejection rates.

“The supply of trade finance, which supports more than 80% of global trade flows annually, has been one of the key constraints to the growth of African trade,” the report says. “The pandemic may be brought under control, but it is already clear that the consequences of this crisis on African trade finance are significant and lasting.”

There is, however, some evidence that non-bank financiers are continuing to step into the gaps left by banks, says Withagen.

“Certainly from the perspective of our clients there is an interest in providing trade finance in the FMCG space,” he says, adding: “Thanks to the digital deal rooms that sprang up due to the pandemic, there are now more solutions for companies to access providers of trade finance than there were a year or two years ago. These digital services, if they existed, were not used to the extent that they are now.”

Trading without borders

In terms of the proportion of intra-regional trade, Africa has long lagged other regions, but the AfCFTA is expected to go some way towards remedying that.

The trade pact, which became operational on January 1, 2021 after being delayed by the pandemic, will gradually lower tariffs on 90% of goods, and – according to officials – could boost intra-African trade by up to 52% by 2025.

That said, there are few signs of any tangible impact on trade as yet.

“The AfCFTA is much-needed in order to get intra-African trade off the ground, but there is some scepticism around how ambitious the plan is and how fast it is moving to implementation,” says Asoko Insight’s Withagen.

A research note by Fitch Ratings puts the issue more frankly. “We believe the removal of non-tariff barriers to trade under AfCFTA is likely to lag behind the agreement’s ambitions, which may blunt its effect. The impact of the East African Community customs union, for example, has been limited by a lack of integration and removal of non-tariff barriers, despite its 15-year history,” says Jan Friederich, Fitch’s head of Middle East and Africa sovereign ratings. “Moreover, regional trade growth will continue to face obstacles. Infrastructure shortfalls, including poor roads and port congestion, remain a substantial challenge.”

But Africa’s comparative lack of intra-regional trade isn’t just caused by trade barriers but by the make-up of its exports – which continue to be dominated by primary commodities and natural resource extraction. This hangover from the colonial era, whereby Africa’s main role in trade was to provide Europe with inputs, will take some reversing.

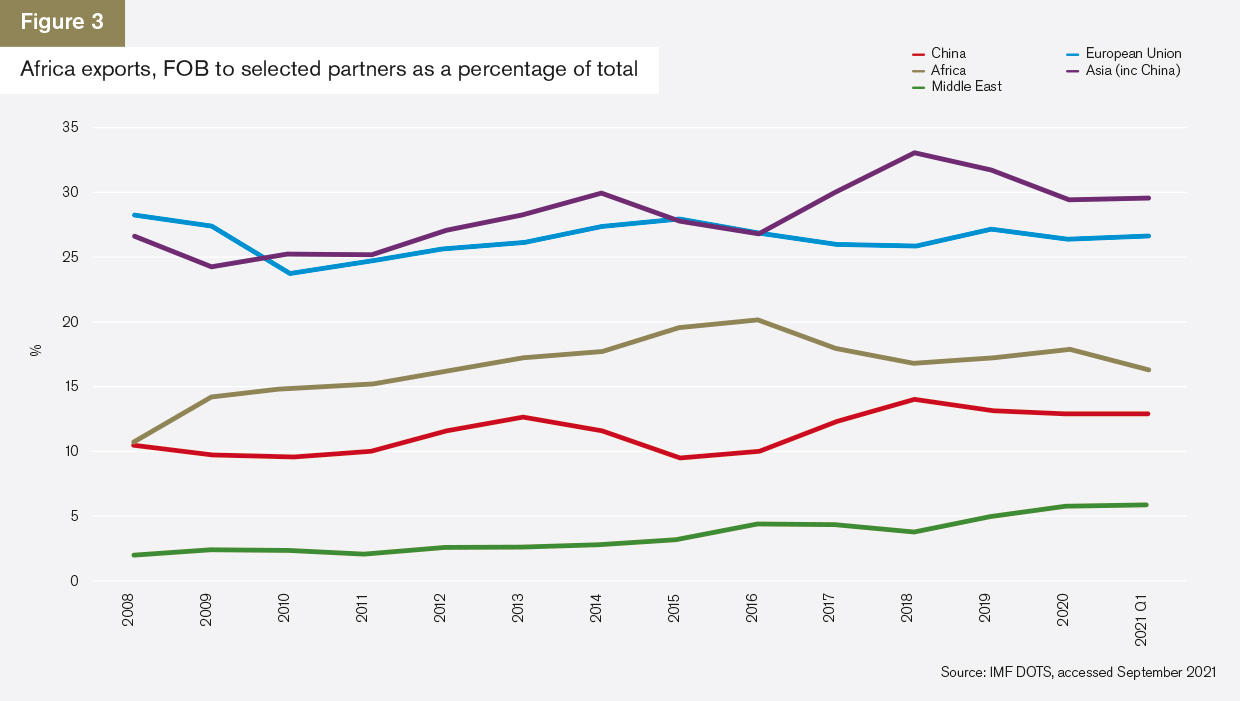

Despite an increase in intra-regional trade since 2008, African countries’ exports to both Asia and the European Union are almost double their exports to one another (see figure 3). Increased trade integration could support manufacturing investment and productivity gains, which would in turn support the development of regional supply chains, but with data from this year putting intra-regional trade in Africa at just 16% of the total, versus 60% and 68% respectively for Europe and Asia, the region has a long way to go.

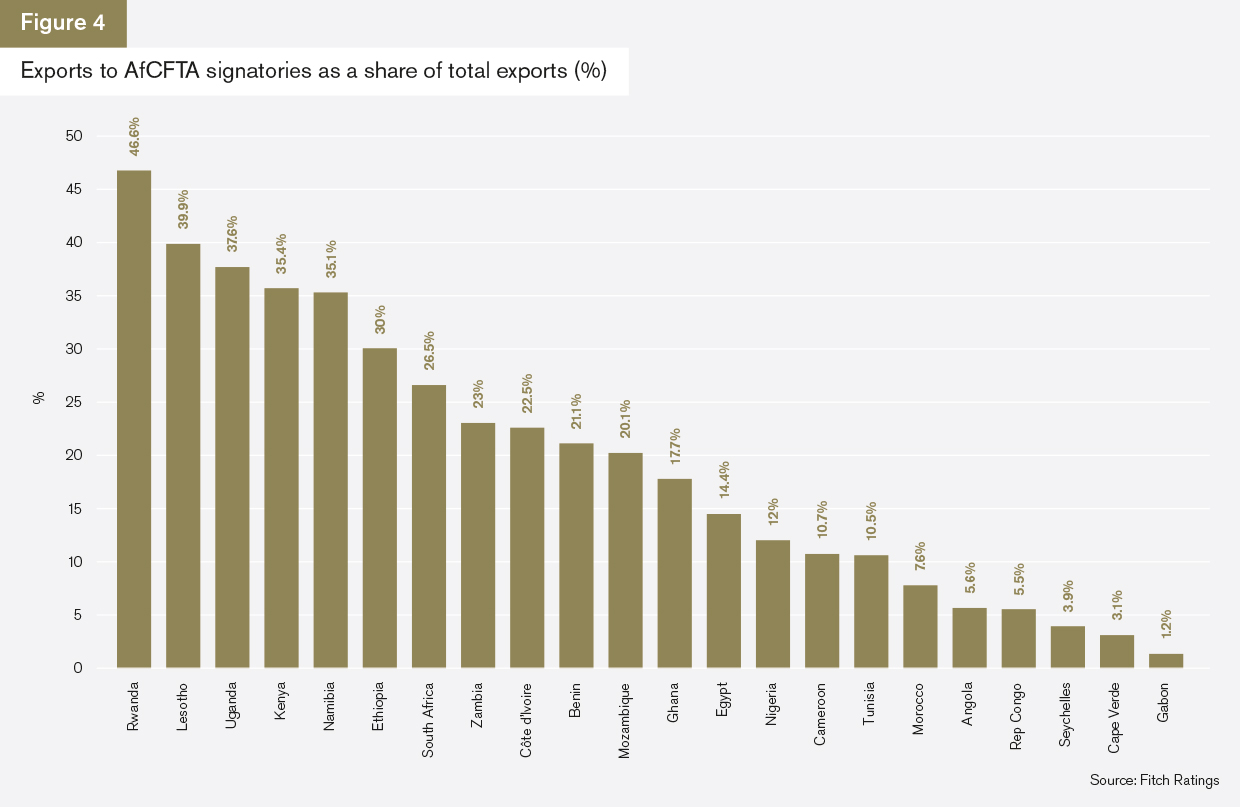

While the data shows that some countries in Africa appear at first glance to be more regionally integrated than others, this should be treated with care. Almost half of Rwanda’s exports, for example, go to other AfCFTA signatories, according to data compiled by Fitch Ratings (see figure 4). A sizeable proportion of exports from Lesotho and Uganda also go to their AfCFTA peers. However, exports from these three landlocked countries, while classified as intra-regional, are most likely destined for re-export outside of the continent.

Expectations that a freshly implemented trade deal would have much impact, especially at a time when Covid lockdowns are still in place and global demand remains volatile, are premature, highlights Signal Risk’s Gopaldas. “Progress will be incremental. We need to realise that the FTA is a journey and not an event,” he says, adding that the European Union’s single market took around 40 years to implement. “There are numerous positive signs, not least the fact that although both human capital and financial resources were stretched last year, the AfCFTA still managed to maintain momentum. This is going to be a long process and is not going to be linear.”

(Another) scramble for Africa

China’s Belt and Road Initiative, the multi-billion-dollar infrastructure investment programme that now counts 46 African nations as recipients after Botswana signed up in January 2021, has changed the shape of African trade over recent years, cementing China as the continent’s largest trading partner.

However, new plans by both the G7 and the US look set to challenge the Asian giant’s primacy in Africa.

Earlier this year, the Joe Biden administration unveiled plans to revamp the Trump-era Prosper Africa initiative as it works to “substantially increase” two-way trade and investment between the US and Africa.

Meanwhile, in June 2021, the G7 launched Build Back Better World, which will see development finance tools used alongside private sector investment to “catalyse hundreds of billions of dollars of infrastructure investment for low and middle-income countries in the coming years”, according to a statement released after the annual G7 summit.

According to Signal Risk’s Gopaldas, this renewed focus on Africa by the world’s wealthiest economies could lead to new opportunities for both trade and investment.

“If we play our cards right in the African continent and negotiate as a collective, there’s an opportunity here. Economic diplomacy needs to be pragmatic. Instead of picking one or the other side, what you need to do is extract maximum value out of each partner who can each offer something different, and it doesn’t just apply to the US or China, it applies to other partners as well,” he says. “A more multipolar world will see a reduction of trade tensions, and hopefully the strategic competition will be important. However, there is a word of caution on that, because Africa as a continent needs to avoid being exploited in the same way it was during the Cold War.”

An uneasy, uneven recovery on the cards

With the most recent figures showing an uptick in African trade as global demand returns, diverse export sectors have the potential to contribute to a recovery from one of the continent’s worst crises in living memory.

Whether this renewed dynamism will hold, however, will depend upon numerous factors, from the success of the implementation of the AfCFTA to the ability of Africa’s governments to contain the Covid-19 pandemic – as well as access to timely and affordable trade finance, be that from banks or from funds, fintechs and alternative lenders.