GTR recently teamed up with law firm Holman Fenwick Willan (HFW) to conduct a survey on the future of the commodity trade finance market focusing of four main topics: the role of securitisation in trade finance, alternative finance, digital solutions and sustainability.

The key finding from the survey, which included feedback from close to 200 respondents, is that the commodity trade finance market is struggling to come to terms with new developments.

“In particular, it is lagging behind in exploiting certain novel payment methods and the rise of alternative finance providers is not mirrored in the actual use of such finance in the lending market,” says Philip Prowse, partner at HFW. “Shifting priorities, such as sustainability requirements, are also adding new challenges for market participants.”

“The question that needs to be addressed is whether, and if so why, there is a reluctance to adapt and whether the tools the market is being offered are simply not fit for purpose, or are not sufficiently understood or available,” he adds.

Background to the survey

What is the future of trade finance? Start-up communities and even global traders are increasingly unable to access traditional sources of finance. Technology and sustainability are becoming increasingly prominent in the landscape.

In conducting this survey, we sought to gather the views of the commodity trade finance market on the future of its business. The survey was comprised of

18 questions covering the four main topics we chose to tackle.

Market participants responded in significant numbers and the results somewhat reflected the uncertainty prevalent in the market. For example, in relation to certain questions there was almost unanimity on points raised, but for other questions, the market was evenly split in its response.

There remains a need to address the barriers in trade finance. Almost half of respondents identified the reluctance of banks to participate in the market as a significant barrier to them accessing commodity trade finance funds. Over a third identified market regulation as an obstacle. Is technology able to overcome these barriers and assist with greater access?

Over half of the respondents to our survey identified that the cost of obtaining trade finance has risen or increased considerably in the last five years. Can technology and the advent of an increasing number of specialised trade finance digital solutions help to overcome the increasing costs? Is alternative finance the answer?

What follows is an excerpt from the survey findings – focussing on securitisation.

Securitisation

Securitisation is not the most obvious vehicle for commodity trade finance. So why is it that we are seeing an increasing number of companies using, or looking to use, the structure?

What is a securitisation?

Essentially, this is when one party (the issuer) issues bonds/notes, into which investors (noteholders) invest. The issuer then uses those sums for whatever activity the bond permits; so for our purposes, commodity trade finance deals. The proceeds received from the underlying commodity trade finance deals are then used to repay the noteholders and any excess is dealt with in accordance with the terms of the prospectus and related documentation (i.e. the contractual basis which sets out the terms and conditions for the notes issuance) which has been issued.

Problems with the securitisation structure

The main problem in using securitisation is often the tenor of trade finance deals compared with the duration of a bond.

Trade finance securitisations to date have often taken the form of one investor becoming the noteholder in relation to one company’s portfolio of trade finance assets. This is relatively easy to manage. The complexity arises where there is an issuer whose sole purpose is the investment of note proceeds in trade finance deals. This issuer will have numerous deals with counterparties, who then themselves have various counterparties.

Whereas a bond programme is likely to run for a year or more (ie three, five or seven years), most trade finance receivables will have a maturity of 60 to 180 days, so there will be a continual need for churn if the bond is to succeed, lest there be unused investment idling away and being unable, therefore, to service the bond payments. However, not all market participants have been deterred – please see the case study for further details.

The securitisation process is also not cheap. The issuing of a prospectus can often cost many hundreds of thousands of pounds in professional advisor fees, much of which will often have to be financed upfront before noteholders become involved. Indeed, our survey reveals that cost is the main issue in deterring market participants from using securitisations. It can also take some time to establish the necessary structures and complete the process of issuing a prospectus, which again can contribute to high costs.

A close second deterrent in our survey is the perception that the securitisation procedure means that there is a lack of relationship with the commodity, because the deals are generally a level removed from the direct investments that are being made. One of the respondents identified their key concern as being a “lack of control of assets in the programme… and the asset conversion cycle”. This can, however, all be avoided through the detailed requirements of prospectus documentation and through carefully defined investment eligibility criteria.

Advantages of the securitisation route

The advantages of using securitisation can be manifold. For noteholders, all the work of sourcing deals is carried out by someone else. The bond issuer will also take care of burdensome regulation, like sanctions, KYC and so on. The prospectus regime is detailed and highly exacting, which means noteholders often feel more comfortable with the structure and risk, irrespective of the expected performance of the underlying assets, even in a turbulent market.

Furthermore, bonds are usually secured in this asset class, so there will be security to enforce in the event of a default, which should mean that noteholders are preferred even in the event of issuer insolvency. A properly secured liability will also be one that will not be subject to the new EU laws on “bail-in” of financial liabilities under the Bank Recovery and Resolution Directive.

For financial institutions, the attraction is the chance to de-risk. They can also widen their risk portfolio, achieving a broader spread of investment across different asset pools.

This aligns with the findings of our survey: when asked what appealed about the securitisation process, the majority of respondents (48.3%) selected the opportunity to de-risk as the main factor.

In essence, the structure offers a complex, defined and managed investment opportunity that was hitherto available in bespoke pre-export structured commodity finance deals, but which has dropped away due to the burdens of cost of regulation.

A method for the future?

There remains a desperate lack of liquidity in the trade finance space. Securitisation may be one method by which investors not normally involved in the commodities markets could be tempted to invest. It may also be another way in which banks can re-enter the market, challenging the common perception that banks are simply not willing to participate in the market (as identified by our survey with 47% of respondents selecting reluctance of banks as the main barrier to accessing finance).

For example, a major European bank in December last year closed the largest trade finance securitisation to date, with a value of US$3.5bn. This was done via a synthetic collateralised loan obligation, which is unfunded, meaning that the assets sold stay on Deutsche Bank’s balance sheet, but the risk is effectively passed to the investors. The third such transaction carried out by the bank, it stated at the time that it intended to use the method again to reduce its risk-weighted assets (and accomplish regulatory relief in this way).

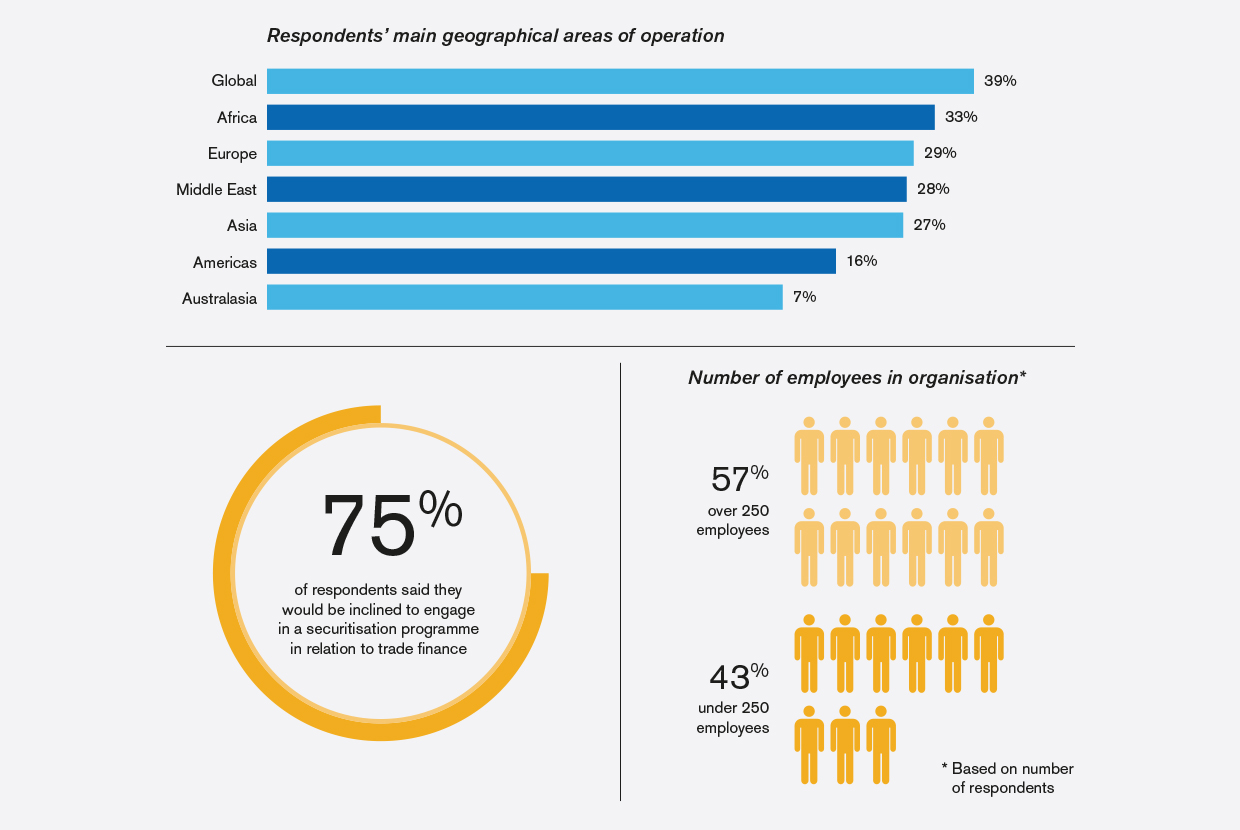

Over half of the respondents to our survey said that they are moderately inclined to engage in a trade finance securitisation programme – an indication perhaps of the market’s willingness to innovate to overcome barriers in accessing finance.

Case study: Synthesis Trade Finance

HFW has advised a client, Synthesis Trade Finance, on the establishment and issuance of a US$500mn bond series for investment in commodity trade finance transactions sourced from various originators.

The bond is being listed on the Luxembourg Stock Exchange and the proceeds from the issuance will be invested in commodity trade finance deals across various geographies and commodity types.

As the underlying investments were the subject of multiple originations, the bond was novel for the Luxembourg listing authorities and the process to have the prospectus approved was complex, but it does demonstrate the willingness of the authorities to co-operate in such novel deal structures and could be an indication that securitisation is a viable structure for the commodity trade finance sector.

We would like to thank everyone who took the time to respond to the survey. The full report can be found here.