Historically a relatively niche working capital tool, inventory finance is coming out of the shadows. Supply chain disruptions and a boom in data centre demand are prompting companies to revisit stock management strategies, and inventory finance provides a diverse set of possible funding structures. But with fraud risk never far away, how can lenders ensure they are staying safe?

After decades of relative stability and growth, the last five years have been tumultuous for global trade, and inventory management is no exception.

Driven on the one hand by technological acceleration – notably explosive growth in data centres and artificial intelligence – and on the other by trade tensions and supply chain shocks, corporates and lenders have been forced to adapt to a new normal.

One consequence is that companies have revisited their strategies around stock levels.

“Inventory has become the silent absorber of uncertainty,” says PwC.

“Companies have built up stocks as a hedge against supply chain disruption,” particularly in sectors with long lead times and where supply chains are less agile, it says in a working capital study published late last year. “During the recent period of uncertainty, we have seen a shift from ‘just in time’, to ‘just in case’, to ‘just because’ stocking.”

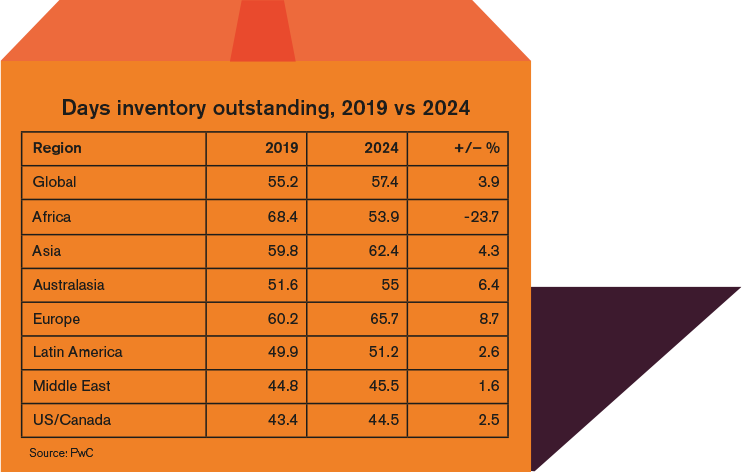

But holding more stock comes at a cost. The study finds that days inventory outstanding – a measurement of the time a company holds stock before it is sold – spiked during the pandemic and has not since returned to previous levels.

“This strategy absorbs capital, raises storage costs and heightens the risk of obsolescence,” it says. “The supposed stability of extra inventory is unreliable – it can disappear quickly into lost value.”

Against that backdrop, inventory finance solutions seem to be maturing, shifting from a relatively complex and difficult-to-implement form of working capital management to a crucial tool for companies seeking to optimise balance sheets and remain resilient in the face of disruption.

John Goodridge, co-founder of Silver Birch Finance and head of its inventory solutions business, says the sector “is a very different place, even compared to just five years ago”.

“Then, we were almost trying to preach the virtue of looking at this,” he says. “Now, companies are approaching us; they already want to do something, and they probably have some ideas in mind.”

A maturing market

Historically, inventory finance deals have often proven to be more difficult to close than those involving traditional trade finance products, or other working capital solutions such as supply chain finance.

“In my view, the single biggest reason that inventory monetisation programmes often don’t go from the term sheet stage to closing and funding is a misalignment of interests and priorities at the customer,” says Massimo Capretta, a partner at Mayer Brown and leader of the law firm’s global trade finance practice.

“Unlike many structured financing transactions, which often can be implemented just by the customer’s treasury function, these solutions deal with physical – and often critical – goods for the customer.”

This requires broader internal coordination, including ensuring a company’s treasury operations are also aligned with procurement, accounting, IT, compliance and tax, Capretta says.

“That means you usually need C-suite involvement and support,” he says. “In my experience, that isn’t going to happen unless there is a C-suite problem to be solved. Just improving working capital efficiency isn’t going to be that kind of problem.”

“Even [for] big companies with very good ratings… that cost starts to become prohibitive, and it’s going to be passed on somewhere.”

Richard Evans, Falcon Group

But in some sectors, industry insiders say this situation is changing. In manufacturing, for example, there has “absolutely” been growing demand for inventory financing solutions in the last few years, says Mike Malone, head of new business development and product management at Netherlands-based equipment financing company DLL.

A subsidiary of Rabobank, DLL uses structured inventory finance programmes to facilitate manufacturers’ equipment purchases.

“Several dynamics” are driving this shift, he suggests. Not only are businesses seeking to hold more inventory closer to end markets, but they also face rising costs, longer payment cycles and a higher interest rate environment.

As a result, floor planning – a form of inventory financing where companies use credit lines for initial stock purchases – is increasingly “under the spotlight”, says Malone. “The days of ‘set and forget’ programmes are over. Rising costs and longer inventory cycles mean manufacturers are taking a much closer look at their terms to protect margins and remain competitive.”

One of the largest drivers of demand is the technology sector. Large technology companies are aggressively pursuing the build-out of hyperscale data centres, requiring vast amounts of specialist equipment such as AI-compatible chips, computing units and cooling racks.

Those companies need certainty that this equipment will be available when needed, but over a long period of time, that certainty “comes at a cost”, according to Richard Evans, head of banking partnerships at Falcon Group.

“That cost has to sit somewhere,” Evans said at the GTR Nordics event in Stockholm last November. “It can either sit on the balance sheet of that hyperscaler, or it sits on the balance sheet of their suppliers.

“Given the numbers that we’re talking about, that creates some serious issues. Very suddenly, even [for] big companies with very good ratings… that cost starts to become prohibitive, and it’s going to be passed on somewhere.”

As a result, tech companies are increasingly turning to companies like Falcon to purchase that inventory and hold it until needed, Evans said. This allows them to secure equipment for future use without holding it on their balance sheets, while their suppliers receive the funds upfront.

When inventory finance goes wrong

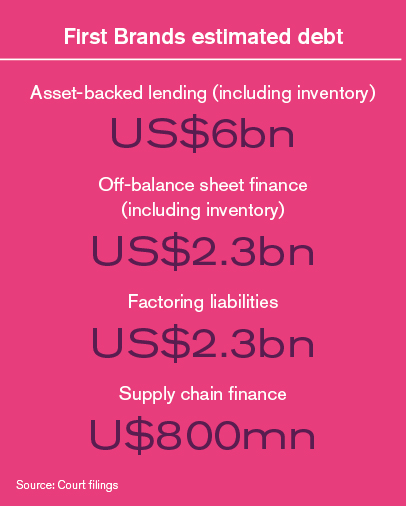

Despite the growing momentum behind inventory finance, it has not been insulated from the fraud scandals that have intermittently blighted the trade finance market in recent years – the most recent being the high-profile bankruptcy of Ohio-based auto parts supplier First Brands.

Since its bankruptcy in late September, several lenders and investors have accused First Brands companies of abusing a variety of inventory-related structures, including off-balance sheet facilities, asset-backed lending and sale-and-leaseback transactions.

The company faces allegations that the same inventory was used to secure financing from multiple lenders, including through double-pledging, commingling and the presentation of falsified documentation.

Across both inventory-linked asset-backed loans and off-balance sheet financing, the company is believed to owe creditors as much as US$8.3bn, and court filings show at least one creditor has accused First Brands of “widespread fraud” in relation to these facilities. Its founder, Patrick James, has denied the allegations and, as of press time, proceedings are ongoing.

But the First Brands scandal does not mean inventory finance is inherently susceptible to fraud, proponents believe.

Kellie Scott, executive director for inventory solutions at Silver Birch, suggests that, based on reports of the scandal, “it seems there was some form of hiding debt, or hiding how leveraged the company was”.

“Then, you have other factors: first, governance from a private credit perspective can be different to the governance you would have with a traditional bank model,” Scott points out.

“Second, from what’s being reported in the press, there may have been commingling of funds, rather than using segregated accounts, potentially [regulatory] filings that weren’t taking place, and generally a lack of rigour around the controls put in place.”

That raises a broader question: is the apparent lack of transparency in First Brands’ case indicative of a systemic issue?

Speaking on condition of anonymity, an expert in the accounting treatment of inventory finance says that, despite relatively established rules on financial disclosures – particularly in the US – “there is an element out there that is in the grey”.

“That is people just pushing the accounting and getting these [goods] off their balance sheets,” they say. “I think the current problem is when transactions are off-balance sheet, you might have to disclose your commitments but you don’t have to say why, how or what your purchase is.”

For Silver Birch’s Scott, another important consideration for funders entering financing arrangements is client selection and product appropriateness.

“Inventory finance is suitable for certain types of clients, and from a bank’s perspective, it’s rarely ever going to be an entry-level product,” she says. “It comes down to knowing your customer, their business and their flows.”

Scott adds that inventory finance transactions can be structured in a variety of ways, which in turn present different types of risk, and many companies active in the sector bear little resemblance to those caught up in the First Brands case.

“A key thing to differentiate is there are many working capital solutions within inventory finance,” she says.

Different structures, different risks

Part of the reason the inventory finance market is so fragmented – comprising a mixture of banks, specialist lenders and private credit investors – is because of the diversity in how deals are structured. Many bear little resemblance to the off-balance sheet structures deployed by First Brands.

In some cases, which often appeal to traditional banks, an inventory finance provider will purchase goods from a supplier and sell them to the end buyer on extended payment terms.

This process typically takes the form of flash title transactions, where the two sales are carried out back-to-back.

“The purpose of this is that banks that cannot or do not want to purchase or hold inventory on their own balance sheet can instead finance the receivable that is payable in connection with the sale of such inventory,” says Tudor Plapcianu, a partner in Norton Rose Fulbright’s structured trade and commodity finance practice.

“If they are happy with the unsecured credit risk of the debtor, they can provide financing without seeking to acquire title to the goods,” he says.

“This is inherently more complex than typical trade finance given the intersection of credit risk, inventory management, operational control and reconciliation, legal entity setup and real-time visibility.”

Andrew Betts, CredAble

In other structures, funders help companies manage existing inventory levels, for instance, by obtaining title to goods stored in a warehouse until they are needed. This can help move inventory off balance sheet and free up working capital.

Andrew Betts, chief growth officer at India-headquartered fintech CredAble, which provides inventory solutions alongside payables and receivables financing, says he is seeing “interest move from flash-title to third-party inventory ownership as a way of transforming inventory optimisation”.

Yet there can be various complications with this approach.

“This is inherently more complex than typical trade finance given the intersection of credit risk, inventory management, operational control and reconciliation, legal entity setup and real-time visibility,” Betts says.

As a result, he says, banks looking to capitalise on growing interest in this area are increasingly partnering with inventory specialists as part of their supply chain finance offerings.

Another important factor is adherence to accounting requirements. Rules vary by jurisdiction, but it can be problematic for firms to remove inventory from their balance sheets if they are contractually obliged to repurchase it, unchanged, at a later date.

This is less of an issue if the goods are commodities that could be sold elsewhere on the market, such as crude oil or LME-warehoused metals. Assuming any price risk is addressed through hedging, the funder is theoretically indifferent as to whether the goods are sold back to the company or into the market.

“In that example, a bank could do a transaction where a commodity trader is not obliged to pay it back, which might mean that trader’s balance sheet is showing cash, not inventory,” says Nick Grandage, also a partner at Norton Rose Fulbright.

“It’s just a convenient means of commodity financing, as it’s quick to implement and quite flexible.”

But where goods are not exchange-traded or fungible commodities, such as equipment that is only valuable to the company holding it, deals “are a bit more complicated”, Plapcianu says.

In that scenario – where funders may be left holding title to goods they cannot readily sell – Plapcianu says the risk begins to resemble a credit exposure to the end buyer.

“That bank has to be happy taking an unsecured credit risk on its client. We’re not looking to use inventory structures to make an unbankable client bankable.”

John Goodridge, Silver Birch Finance

“Ultimately, you’re looking at the repurchase or liquidation obligations from the end client, not the inventory itself. The main point is that there is real inventory and there are real trades,” he explains.

In terms of risk, this means banks often provide inventory finance to existing clients, sometimes through an intermediary, Silver Birch’s Goodridge says.

“That bank has to be happy taking an unsecured credit risk on its client,” he says. “We’re never looking to use inventory structures to make an unbankable client bankable.”

Even then, there is always a risk that the underlying borrower is committing fraud. In the 2020 scandal involving oil trader Hin Leong – which drew billions of dollars in financing from numerous large banks – it emerged the company had double-pledged and commingled oil inventories supposedly held in storage.

For Plapcianu, the issue comes down to good governance and risk controls, as with any form of financing.

“The trade finance industry is in general considered a safe and well-performing industry. However, it remains subject to the risk of fraud, and there have been a number of recent high-profile examples,” he says.

“It is advisable that financiers consider what minimum checks they may want to undertake to reduce the risk of double-financing of assets or the risk that assets being financed do not actually exist.”