Concerns over the Iran conflict’s ripple effects across African economies are rising as the war continues to hit key commodity trade corridors.

Countries across the African continent are feeling the impact of the war between Iran, the US and Israel, as the ongoing attacks put a strain on shipments of key commodities such as gold, oil and fertilisers, according to specialist intelligence advisory Pangea Risk.

Many African nations are highly dependent on imports of energy and fertilisers, needed in agriculture and food production, and on exports of gold and other minerals such as diamonds.

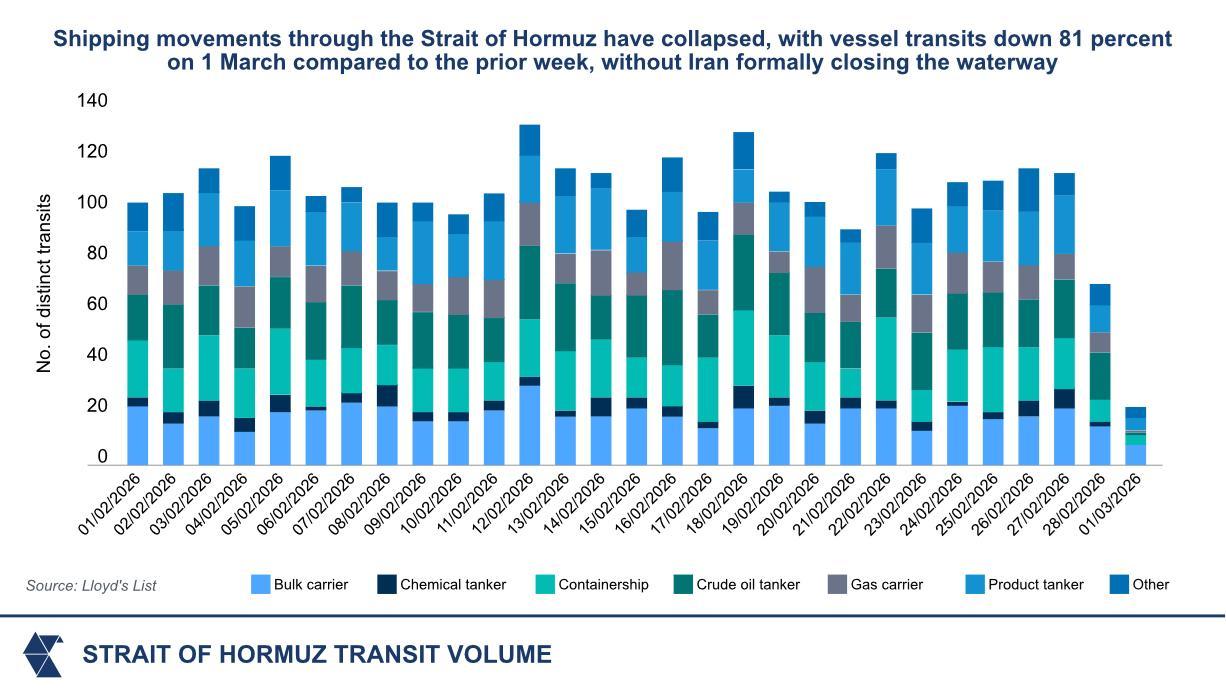

But with vital supply routes such as the Strait of Hormuz now brought to a near halt, the effect on commodity markets is contributing to the return of inflation in African economies, Pangea Risk CEO Robert Besseling told attendees at last week’s GTR Africa event in Cape Town.

“This is unfortunate, as many African countries had been bringing inflation down,” he said. “We are likely to see more volatility in inflation and interest rates” going forward because of the Middle East disruption.

A report from research group Economist Impact earlier this week also confirmed that countries such as Kenya, Uganda, Nigeria and the Democratic Republic of the Congo (DRC) were particularly exposed to economic shocks resulting from the conflict because of their reliance on energy and fertiliser imports.

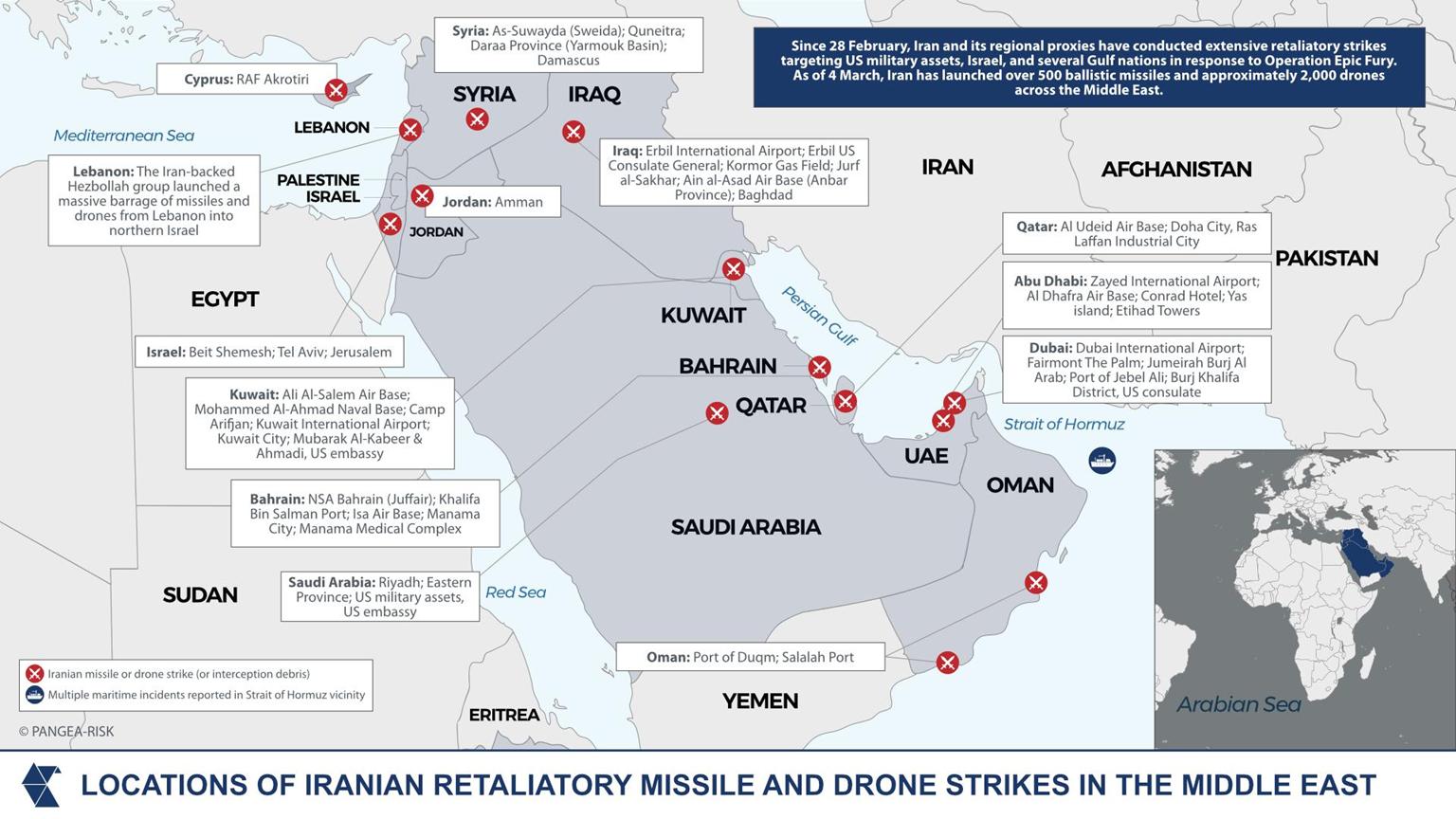

The Strait of Hormuz, where shipments are currently largely halted due to a series of attacks in the region, accounts for a third of the seaborne fertiliser trade, according to UN Trade and Development.

Saudi Arabia is a leading exporter of phosphorus and nitrogen products, while Qatar and Oman operate massive ammonia and urea complexes.

Pangea Risk also noted that this could “create opportunities for Morocco to step in, as it did during the Russia-Ukraine war”.

At the same time, disruption to other African-produced commodities such as gold and diamonds is already taking place in countries including the DRC, Ghana, Tanzania and Zimbabwe, which are unable to fly their gold shipments on Emirates flights to Dubai, according to Pangea-Risk.

“In Botswana, the government is holding twice the authorised level of diamonds because they cannot be shipped to the UAE and to Indian processing sectors,” Besseling said.

“So this is the immediate impact: many of Africa’s gold producers cannot benefit from record-high gold prices because they are unable to ship the product.”

Meanwhile, a reduction in the supply of oil from the Middle East could be “good news for some African oil exporters”, Besseling said, with Angola set to “see a benefit of 3.3% on its current account if oil prices remain at these levels and if it can maintain production”.

“However, Angola is also exposed as an importer of goods and therefore to inflation, and will likely bring back some fuel subsidies it has been phasing out,” he added.

Other African countries without sufficient refining capacity, like South Africa, could see supply shortages and additional increases to petrol prices across March and April.

On the other hand, Nigeria – which has invested heavily in refining and revoked import licenses to multinationals to ramp up domestic usage – is set to benefit from higher oil prices and increased output, according to Pangea Risk.

The intelligence advisor predicted the war is “unlikely to be long” due to the extreme effects on global commodity markets.

“We are starting to see that the current conflict, at its frequency, intensity and geographical expansion, is unsustainable for all actors involved,” he said. “Therefore, the baseline scenario is a short-lived, high-intensity war lasting up to three weeks, followed by a slower tempering phase of up to two months.”

Debt, capital inflows and risk perception impacts

Beyond the effect on commodity markets, promising growth in Gulf investments in Africa – including in ports, logistics, energy and aviation – “may scale back as they refocus on domestic security”, Besseling warned.

The Middle East conflict is also set to have implications for debt, capital markets and credit ratings across Africa, he warned, as the two regions are “deeply intertwined”.

“African sovereign bond spreads have jumped more than those of other emerging markets”, he said, which suggests the war is reinforcing an existing “risk perception problem” for the continent.

“This creates both risks and opportunities – there are high yields in African trade and project finance, but financing must remain sustainable to avoid future debt crises,” he told GTR Africa attendees.

“Export credit agencies and development finance institutions have an important role to play. Africa faces a US$90bn debt wall this year, and many countries cannot absorb more hard currency debt. Mobilising local capital will be critical.”