One of the greatest unresolved challenges facing Africa’s agribusiness sector is the lack of value addition. Sub-Saharan Africa-focused consultant Dr Edward George looks at how this affects two of Africa’s most important soft commodity value chains – cocoa and cotton – and explores how the fostering of local demand for crops could transform the balance of power for Africa’s agricultural producers.

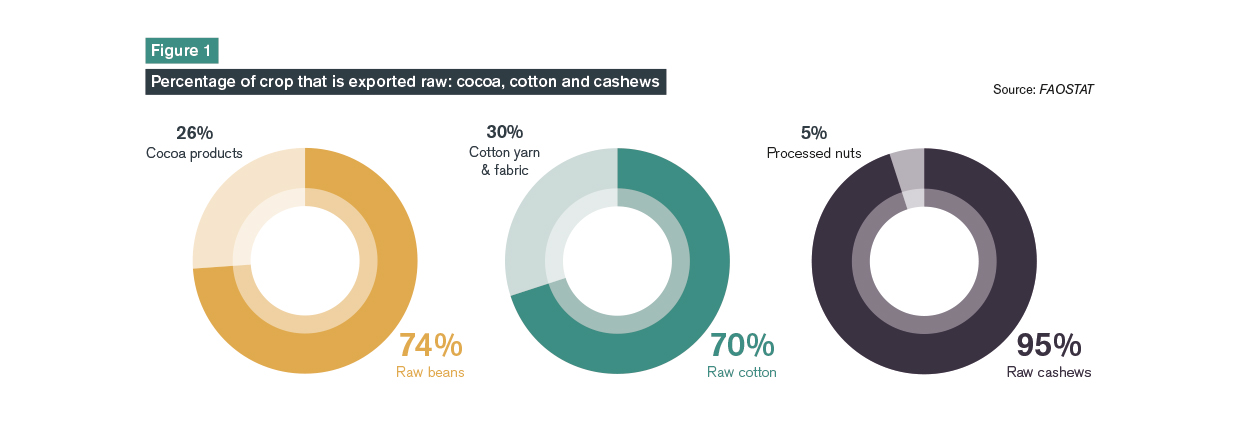

Of all the challenges facing Africa’s agribusiness sector, the failure to add value to crops before they are exported has proved the most intractable. Most African softs are exported raw to global markets, and the processing industries that do exist locally struggle to add value. They may bring national prestige but they require costly subsidies to survive and create little employment. This situation is acute for three of Sub-Saharan Africa’s most important cash crops – cocoa, cotton and cashew nuts – which provide a livelihood for millions of Africans (Figure 1).

West Africa is the world’s largest producer of cocoa, with Côte d’Ivoire, Ghana, Cameroon and Nigeria producing over 70% of global output. But around 75% of the crop is exported as raw beans to Europe and Asia, with only a quarter staying in the region for processing into cocoa butter, powder and (a little) chocolate. This leaves the lion’s share of value addition to be captured by the confectioners and retailers at the end of the chain.

Cotton is another mainstay of West Africa’s agricultural sector, yet 70% of the crop is exported raw to Asia where it is processed into yarn and fabric and re-exported back to Africa. This means there may be West African cotton farmers wearing Asian-manufactured shirts made of the cotton they grew themselves. And, in the case of cashews, barely 5% of the crop is processed prior to export, with 95% of nuts going raw to India and Vietnam for processing and consumption.

It is not that there is no processing of cash crops in Africa. The problem is that most processing is basic. The majority of cash crops go through the bare minimum required for export or sale to the next part of the value chain. Although this can bring in immediate cash for farmers and processors, it means that they put in all the work to make a fungible commodity that is easy to trade and then let all of the value add go to those further down the chain (see fact box, page 29).

Processers struggle to compete internationally

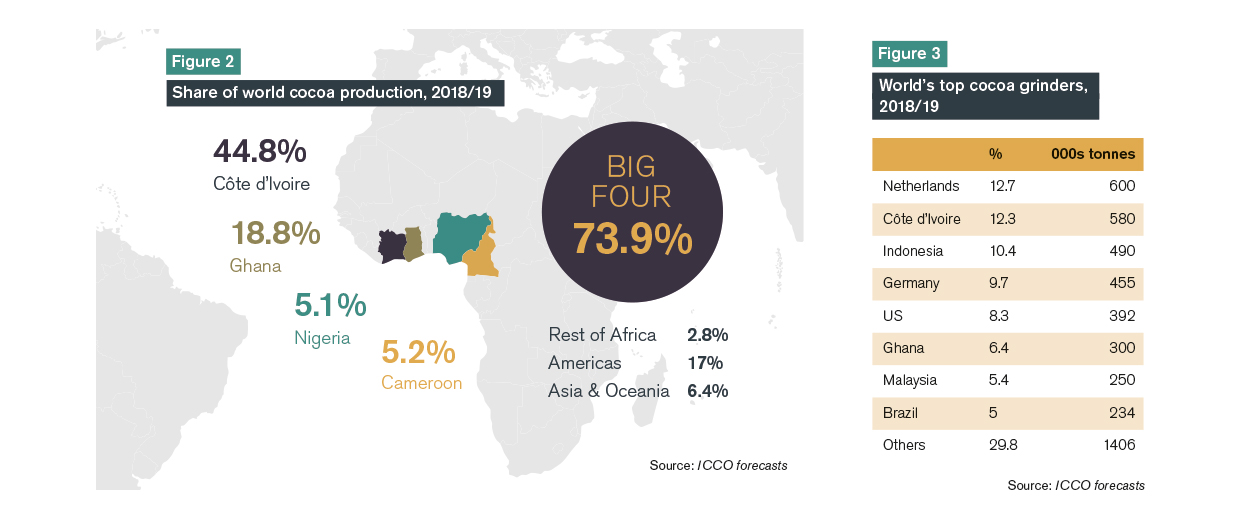

There are processing sectors in Africa that extract more value from the crop, notably in cocoa and cotton. West Africa is one of the largest cocoa grinding regions in the world, accounting for 20% of global output. As the world’s largest producer of cocoa, Côte d’Ivoire has long vied with the Netherlands to be the world’s largest grinder, and the Ivorian government has pledged to boost local grinding from an estimated 27% of the crop in 2018/19 to 40-50% in the medium term.

But these strong numbers and ambitious targets belie the challenges facing West Africa’s grinding sector. Despite investment and local abundance of the crop, West African grinders have struggled to boost output and they are losing market share to grinders in Indonesia and Malaysia. They have survived thanks to local subsidies, whether in the form of tax breaks and cheap access to finance or export contracts, price stabilisation mechanisms or guaranteed discounts on the mid/light crop. In Ghana, for example, Cocobod gives a discount to local grinders for beans produced in the light crop (May-August) which are typically smaller and of lower quality than beans produced in the main crop (September-April), most of which are for export. This is not in itself wrong, as all value addition sectors enjoy some form of domestic protection around the world. But across West Africa the system has become so complex and opaque that it has distorted the local market and made it difficult for grinders to operate profitability and sustainably (Figures 2 and 3).

Francophone West Africa also boasts two cotton giants – Sofitex (Burkina Faso) and CMDT (Mali) – which run sophisticated value chains in the region. But they too have had their challenges. Sofitex was forced into a costly and disruptive withdrawal of the Bt cotton (genetically modified pest resistant) variety it was growing when it was discovered that the fibre lengths were shorter, which reduced the cotton’s value and quality.

The revival of the Africa’s textile sector has also been patchy, with the success of new manufacturing hubs in East Africa contrasting sharply with stagnation in West Africa’s textile processing. In the case of cashews, local processing has failed to keep pace with the dramatic expansion in production in Côte d’Ivoire, which is on track to become the single largest producer in the world. This is wasting a huge opportunity to capture value.

Why is value addition so low?

So why is value addition so low in Africa, when the continent’s agricultural sector has so many inbuilt advantages? These include abundant agricultural land, a rapidly growing population, the lower cost of capex for industrial plants, lower labour costs, plus less onerous know your customer and regulation. But many factors work against these advantages.

A key constraint is the lack of an efficient marketing infrastructure. This prevents farmers and processors from getting full value from their crop, even in its raw form. The problems start with the lack of farmer credit and inputs, and progress through the value chain with inadequate storage facilities, poor roads, overloaded ports and lack of access to buyers. This results in high crop losses – typically 30-40% of African crops rot before they reach market – and poor co-ordination between farmers which creates market gluts – as often happens in Nigeria’s tomato sector – and results in farmers getting little or nothing for their crop.

Africa’s agri value chains are highly fragmented, with numerous middle men adding costs while bringing dubious value and high levels of fraud. This creates an unstable platform for setting up processing businesses that rely on regular and guaranteed flows of raw commodities in order to meet the demands of their offtakers.

Taken together, these factors make it difficult for banks to finance value addition in the agricultural value chain. Too many banks have been burned by lending to small processors, traders and co-operatives, when they failed to understand the complexity of local markets and value chains. For many banks the risks are simply too high, from whether the farmers will provide the crops in return for credit advanced by the processor, to whether the processor will get a fair price from traders who are fighting to protect their own margins.

And, in the case of a default, what collateral do local processors really have? Leaving aside the internationally-owned value chains, which operate in their own enclaves, most African processors have ageing machinery and basic warehousing of little or no value. As a result, most banks do not finance the agri sector directly and the funding available for value addition projects falls well short of demand.

Starved of funding and struggling with a fragmented value chain, Africa’s processors face a further challenge: international competition. Cocoa butter produced in Côte d’Ivoire or Ghana directly competes with butters from anywhere in the world. If the costs of power, storage, transportation and paperwork delays are much higher in Africa than in other emerging or developing markets, then domestic processors cannot compete.

Boosting local demand is the key

The key to breaking this logjam is boosting local demand for cash crops, both within countries and regionally. If a country decides to add value to a product for which there is no local demand – for example making cocoa butter and powder – then it must offer a fiscal incentive to local processers. This means subsidies, and any subsidised industry can come to rely on subsidies in order to remain commercially viable, undercutting its competitiveness. But if there are multiple uses, consumers and markets for a crop, this gives market power to exporters as they do not have to take the first price offered to them.

Africa already has a successful example of this model in Ethiopia’s coffee sector. Ethiopia is Africa’s largest producer of Arabica coffee, with output of 7.7 million 60kg bags in 2017/18. But Ethiopia’s coffee exports are smaller than its rival, Uganda, whose output is a third lower. This is because Ethiopia consumes half of its crop (coffee is central to Ethiopian culture), reducing its availability for export. This enables the country to be selective in its coffee exports, helping build speciality brands like Yirgacheffe which command a premium.

Coffee consumption by Africans is also growing, helped by the bean’s brand association with Western working and social lifestyles, and there is ample space for the growth of African brands that meet local tastes and social habits.

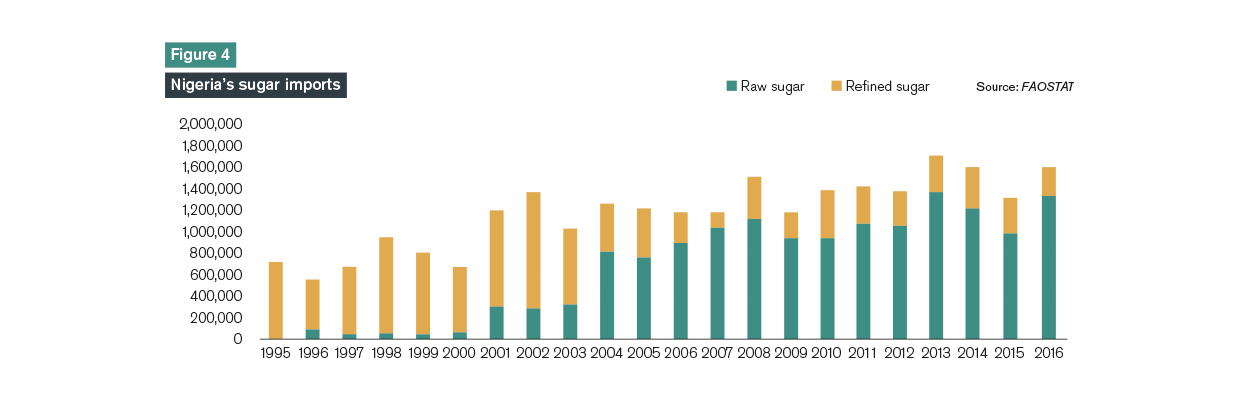

It is also possible to capture the value of crops not grown in Africa but which are – again – intended for local or regional consumption. Nigeria’s sugar sector is a successful example of reverse integration. Starting in the late 1990s the Nigerian government first banned imports of packaged sugar – in order to boost investment in local packing plants – and then started to squeeze imports of refined sugar, while offering incentives for companies to invest in local sugar refineries. The results have been dramatic.

Imports of raw sugar have surged from just 1.2% of sugar imports in 1995 to 83.5% in 2016 (according to the Food and Agriculture Organization of the UN), all of it feeding the growth of the world’s largest sugar refining complex around Lagos. Over the same period, imports of refined sugar have fallen from 1.1 million tonnes in 2002 to just 267,000 tonnes in 2016. This means that all the value previously captured by sugar refiners in Brazil is now being captured in Nigeria. The next step is to make Nigeria self-sufficient in sugar production and redirect the sugar refined from Brazilian raw imports to sub-regional markets such as Ghana, Côte d’Ivoire and Cameroon. (Figure 4).

Similar value-add models focused on local consumption could change the picture for crops like cocoa. Little cocoa is consumed in Africa and the usual argument given for this is that chocolate is not suitable for tropical climates. But it doesn’t have to be chocolate. There are a host of foods and drinks, including cakes, biscuits and soups, that can be produced from cocoa for the local market. Cocoa can even be marketed as a health food, breaking the bean’s association with sugary confectionary.

When I proposed this idea to a Ghanaian friend he put it to his WhatsApp community and was deluged with traditional cocoa recipes, none of which were chocolate, from their aunts, grannies and parents. If cocoa-based products can be developed to suit local tastes and eating habits, it can create a local source of demand for cocoa. This will give power back to the farmers and co-operatives, who will have an alternative market for their beans when international prices and demand are low.

It is in this context that the African Continental Free Trade Area (AfCFTA) could help transform the value addition debate in Africa. AfCFTA’s focus on intra-regional trade – as opposed to international exports – could provide the framework to build cross-border agricultural value chains. These could link together production and consumption zones across Africa and process the commodities in the most efficient hubs. Not only would this put Africa’s value addition industries on a more stable footing, but it could help integrate all the actors into the agricultural value chain, in particular the farmers. This would make it possible to ensure that value addition industries not only add value to the economy but also that they transfer a fair share of this value to all participants in the agri value chain.

Value addition in Africa’s soft commodity sector

Basic processing:

- Cotton lint

- Raw cocoa and coffee beans

- Natural rubber

- Crude palm oil

- Rice, maize, cassava

- Raw sugar

Semi-finished:

- Cocoa liquor, butter and powder

- Roasted coffee

- Refined and fortified sugar

- Maize and cassava flour

- Parboiled rice

Finished:

- Textiles and footwear

- Chocolate and ice cream

- Freeze-dried, instant and ground coffee

- Processed foods (pasta, noodles, bread)

- Tinned fruit and vegetables

Dr Edward George (aka ‘Tedd’) is a consultant on disruptive technology and emerging markets, with a focus on Sub-Saharan Africa. He advises on fintech and agritech projects in the region and is a regular speaker at conferences and commentator in the media (see @DrTeddGeorge for details). Tedd has a number of specialities, including disruptive technology (especially fintech, blockchain, agritech and regtech), soft commodities and agribusiness, trade and trade finance.