The current wave of protectionism, which has seen the imposition of new tariffs and other trade restrictions, will cost the global economy as much as US$10tn in GDP by 2025, according to a new report from HSBC and Boston Consulting Group (BCG).

The report, titled The $10 Trillion Case for Open Trade, was released today for G20 governments, and quantifies the collective economic implications of the choice between rising protectionism and liberal trade policy reform. It uses the BCG Global Trade Model to calculate the outcomes of four scenarios on international goods trade flows for G20 members, excluding the European Union but including France, Germany, Italy and the UK as individual countries.

The four scenarios cover a spectrum. The first scenario, “open and fair trading”, represents the highest plausible level of unfettered fair trade, with an effective World Trade Organization (WTO) making it viable. The second scenario, an “incrementally improving trading system”, derives from a less ambitious set of trade-opening policies, with small levels of improvement each year. A third scenario, the “baseline” case, amounts to a continuation of current trade policies for five more years. Meanwhile, the fourth scenario, “rising protectionism”, assumes a continually expanding use of tariffs and other trade barriers.

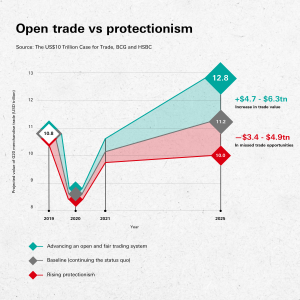

The most illuminating insights come from a comparison of the two most extreme scenarios – the first and the fourth. According to the research, at first, in both scenarios, trade volume rises in 2021 from its 2020 numbers, as the world economy begins it recovery from Covid-19. However, this soon levels off in the “rising protectionism” scenario, with the figures pointing to a plateau by 2022.

By 2025, the difference in economic vitality suggested by the data is dramatic. In the “open and fair trading” scenario, the G20 economies would enjoy a five-year cumulative positive material impact in trade value of US$4.7-6.3tn over the baseline scenario, depending on just how quickly the global economy recovers from Covid-19. This represents an increase of almost 30% in the global trade value of goods exported versus today. Meanwhile, in the “rising protectionism” scenario, the G20 countries would endure a cumulative five-year lost opportunity in trade value in a range of US$3.4-4.9tn.

The difference, therefore, between the best-case and the worst-case scenarios, pandemic recovery pace being equal, is almost US$10tn.

“In a global economy that is already struggling with the impacts of the Covid-19 pandemic, our analysis shows that open trade delivers benefits to every country, as well as to the overall global economy,” says Sukand Ramachandran, a BCG managing director and senior partner. “The additional growth we calculate from open trade translates into jobs around the world.”

According to the WTO, import-restrictive measures implemented since 2009 and still in force affect about 10.3% of G20 imports, worth about US$1.6tn, and the figure is growing. In its latest monitoring report on G20 trade measures, released in June, the WTO found that between October 2019 and May 2020, G20 economies put in place 31 new trade-restrictive measures which were unrelated to the pandemic. The trade coverage for these new import-restrictive measures is estimated at US$417.5bn – the third highest value recorded since May 2012.

These developments are provoking concern that global trade may be closer to achieving the “rising protectionism” scenario identified in the HSBC report than the “open and fair trading” future.

“For the past few years, in many parts of the world, a protectionist mindset has been challenging the continuing trend of globalisation. This mindset, if it spreads further, could endanger the many benefits of more open international trade – which include allowing multinational supply chains to become more flexible and versatile, giving consumers throughout the world better selection and lower prices, and helping pull hundreds of millions of people out of poverty,” the report says.

To right the course, HSBC and BCG have come up with a series of recommendations, which they will have presented to the G20 ahead of the Trade Ministers Meeting on September 22. Among them are calls to strengthen the WTO, create a better global trade rulebook with more effective means of enforcement, promote the positive social and environmental effects of open trade, and develop universally accepted standards for digital trade.

“The B20 Trade and Investment Taskforce has developed a consensus set of bold and ambitious policy recommendations for the G20 to adopt that chart a clear path for inclusive and sustainable growth,” says Natalie Blyth, HSBC’s global head of trade and receivables finance. “It’s critical that trade play its part in securing the post-Covid-19 economic recovery – and more open policies would give the global economy a head start measured in the trillions of dollars.”