Never mind the sanctions, what is also affecting Russian trade is oil price-driven exchange rate volatility. Sofia Lotto Persio reports.

Russia’s economy was accustomed to being in turmoil and under scrutiny, even before the imposition of the Ukraine conflict-related sanctions and the fall in commodity prices in 2014. Ever since 2012, the country’s economy has experienced a downturn due to a number of factors, from weak export demand to a fall in investments. The sanctions and the fall in the price of oil and gas, the country’s main exports, completed the picture: “This is kind of a perfect storm. It is hard to distinguish the single effects, but it is clear the sanctions have had an important one,” Alessandro Terzulli, chief economist at Sace, tells GTR.

The sanctions are still a very sensitive topic. Every institution GTR spoke to for this article was keen to declare its strict compliance with the regulations – so much so that some were wary of discussing the topic altogether. “Banks are much more cautious, they worry about US sanctions as well as EU sanctions. They are wary of what happened to some banks for the Iranian sanctions: they don’t want to risk losing the US market. It is difficult to get financing for Russia: some projects have been delayed, not only due to uncertainty, but also due to this,” says Terzulli.

According to him, being an export credit agency (ECA) makes Sace more accustomed to dealing with difficult situations, and having a good knowledge of the country has allowed the ECA to keep financing deals to Russia, which remains its number one country in terms of exposure: “It is business as usual, but considering all the limitations of the sanctions, some exports cannot be done. Some others need authorisation from the government, due diligence may take longer and the process of authorisation may take longer, and we are more cautious on the risk.”

Commerzbank is one bank that has not shied away from the Russian market. “We had a closer look at what is allowed under the existing sanctions regime and where we have found these niches, we have remained active there,” says Jochen Anton-Boicuk, the bank’s team head for export finance for Central and Eastern European (CEE) and Commonwealth of Independent States (CIS).

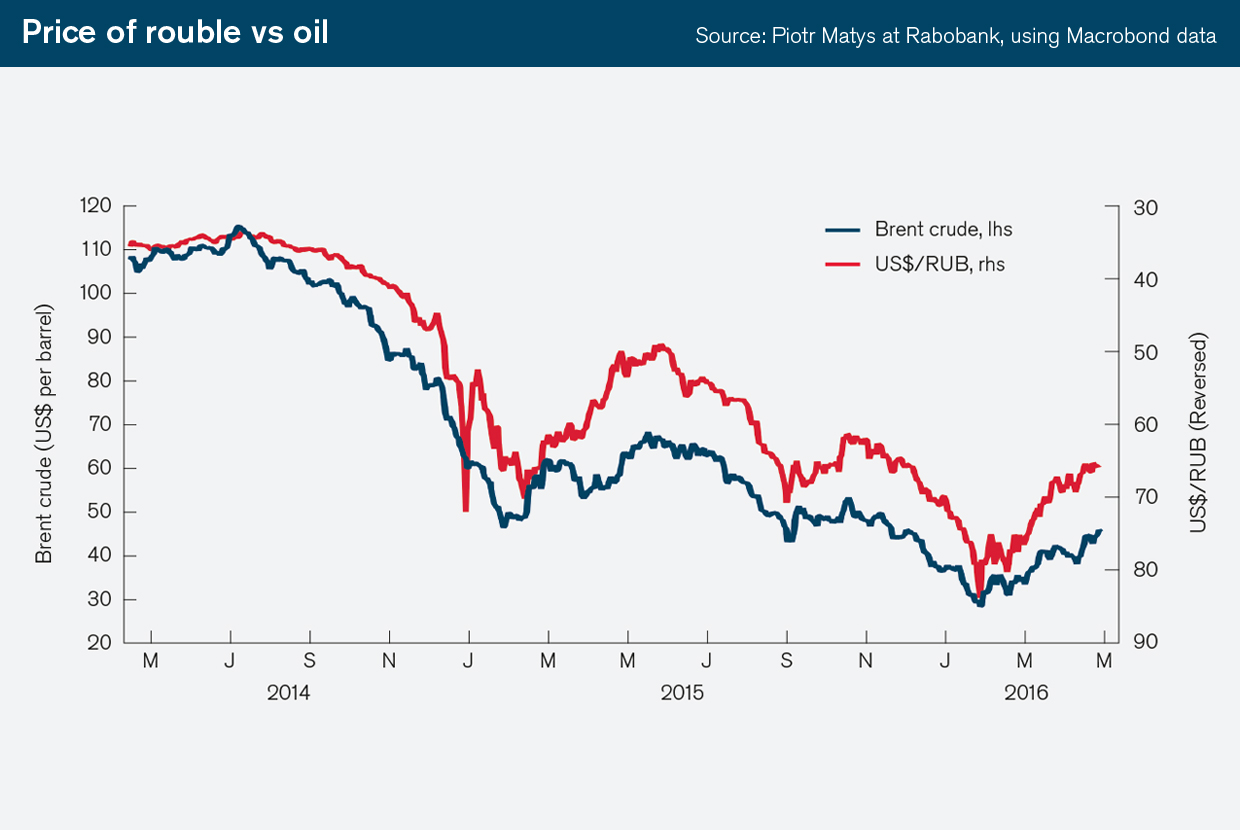

According to him, sanctions have caused delays and cancellations, but they are not the end of the story. “[These were] much more affected by the currency exchange, the devaluation of the rouble, which has had quite a substantial impact.”

Currency uncertainty

Sanction-driven uncertainty stabilised once it became clear which deals could be concluded, but commodity price instability is much harder to tackle. “Given the significance of oil prices for the Russian economy and, subsequently, Russian trade flows, a stabilisation of commodity prices would take much pressure off the rouble and thus be a necessary precondition for gaining a more predictable basis for calculating investments in Russia,” says Anton-Boicuk.

The Russian rouble has been on a downward path since mid-2014, reaching a historical low against the dollar in January this year. Terzulli defends the Russian central bank’s management of the exchange rate, saying it helped the country maintain some sort of financial stability, as well as preserve much of its foreign reserves. “That said, the situation remains difficult, the low oil prices are here to stay. Before the oil prices go back to the levels at which the financial budget in Russia breaks even, it will take time, and I think everybody can agree on that,” he says.

Even with oil prices returning to a sustainable level for the Russian economy, the country would still need to carry out reforms to address structural issues to diminish its dependency on oil and gas, enhance its diversity and develop a stronger manufacturing sector. To do this, Russia needs foreign investments, but this is another challenge, as these have faltered due to concerns about bureaucracy, corruption and transparency. “If things do not change in terms of reforms, foreign investments won’t grow, and this is an important factor in helping to diversify the economy away from commodities,” Terzulli says.

Uncertainty on the currency side has led importers and exporters to seek solutions for further devaluation, if necessary. “When such importers previously would have gone it alone to get a rouble loan, possibly in connection with some hedging instruments, we now have recognised importers seeking such comfort increasingly with Russian banks,” says Anton-Boicuk.

In Russia, VTB has seen an increased demand for trade finance products. According to Igor Emelyanov, VTB managing director trade and export finance, the bank’s trade finance business is increasing because it provides deeper penetration of trade finance products to its largest clients. “We are actively pitching these products to our existing corporate clients, educating them on how to use them effectively and what specific advantages they have,” he tells GTR.

To Asia and beyond

As foreign trade decreases, and business with the European Union is hindered by the sanctions, banks and corporates are looking eastward, focusing more on Asia and, in particular, on China. This pivot to the east has begun to change Russian exporters’ attitudes to foreign currencies for their deals. “Three years ago our clients would be sceptical if we proposed renminbi (Rmb) financing to them, but today the reaction is different. We are often asked to provide quotes in dollars, euro, roubles and now in Rmb as well,” says Emelyanov. “The Chinese and Russian markets are getting more and more integrated, we clearly see this trend. The situation has changed from what it was a couple of years ago, when the choice of the currency was obvious.”

But for small and medium enterprises (SMEs), accessing finance is increasingly challenging. The spike in interest rates has hindered their ability to access loans, not only due to the cost of finance, but also because of the requirements needed. Nikolay Shapilov, head of exports at LogPro, a Russian SME exporting food products, construction materials and machinery, thinks there is a lack of support, considering that his company’s main export destinations are countries in Africa, Latin America, Southeast Asia and the CIS.

“These are not the most reliable partners. Dealing with them means that you should be flexible in your requirements to their financial accounts, to their financial requests, to their credit worthiness, etc,” he tells GTR.

Adapting financing products to cover exporters going into those regions is of paramount importance for financial institutions willing to support Russian exporters. “These are the markets on which we will focus for the next years, but they are unpredictable: most of them have fluctuations. Exporters will avoid putting all their eggs in one basket. Russian companies will diversify their markets,” explains Shapilov.

According to him, banks need to adapt to this too. “[Russian banks] have no other option, for sure we will orient towards these countries. This is not their desire, but it is the situation we are in at the moment and they will have to handle these risks,” he says. At VTB, all eyes are firmly set on Asia. “Asia is a top priority for our clients and for us. We also definitely have plans to increase our trade and export finance business in Africa and Latin America, but it will take some time,” says Emelyanov.

Time indeed will be needed to develop business relations in new markets. “It takes two to three years for a company with experience in international trade to develop a net of sales and exports to Asian countries, so one cannot expect that this would happen like magic,” says Shapilov. Over that timeframe, there may be changes to the sanctions regime and in the attitudes towards Russian business on the European side. According to Terzulli, this is starting to happen already: “There has been a bit of a recovery of that confidence, though not at the levels it was before the sanctions or tensions with Ukraine, but it is gradually coming back,” he says.

To understand just to what degree relations will improve, one has to follow politics and diplomacy: the Minsk II talks between Russia, Ukraine, France and Germany have had a direct impact on the duration of the sanctions regime. Analysts expect the sanctions to be reconfirmed in July and bankers tell GTR that this will remain one of their concerns when looking to the next 12 months at least.