Enforcement of laws that aim to stamp out forced labour is increasingly creating trade and geopolitical risks for companies, a report has found, as authorities interrupt billions of dollars’ worth of goods imports.

Legislation such as the US’ Uyghur Forced Labor Prevention Act and Canada’s forced labour import ban are increasingly working as “de facto trade controls across borders”, according to global risk data company Verisk Maplecroft’s latest supply chain risk outlook.

Authorities are now detaining shipments with little warning for reasons that may be driven more by political motivations, the report said.

James Allan, head of corporate risk and sustainability at Verisk Maplecroft, said: “The blind spot for many companies is that enforcement risk does not map cleanly to supplier-level labour risk.

“Even businesses with limited direct exposure can face sudden disruption if regulators target a product, a country or an upstream link in the supply chain.”

Between June 2022 and February 2026, shipments worth US$3.94bn from multiple industries were detained by US Customs and Border Protection for forced labour concerns.

But the report stressed that while forced labour law enforcement is rising worldwide, it is not happening “in a predictable way”, meaning the risks are likely to be underestimated because they may not fall under typical due diligence processes.

As a result, forced labour risk is shifting from an ethical and compliance requirement to becoming “the newest geopolitical risk” for value chains.

This is particularly visible in the US, the report said, where the government launched investigations earlier this year into the efforts of 60 economies, such as the UK and the EU, to enforce bans on imports linked to forced labour.

The investigations “established a basis for imposing tiered, double-digit tariffs” on imports even from countries that are not ranked as high risk, according to Verisk Maplecroft’s forced labour index.

“This raises a practical question for companies: where will enforcement be influenced by geopolitics, not just forced labour risk?” the report said.

Procurement teams should “take a dual approach” to their supply chains and consider where they are exposed to forced labour risk as well as if an “enforcement event is likely due to geopolitical considerations”, the report advised.

They should also locate their most critical exposures and the inputs where disruption would have the biggest impact on operations.

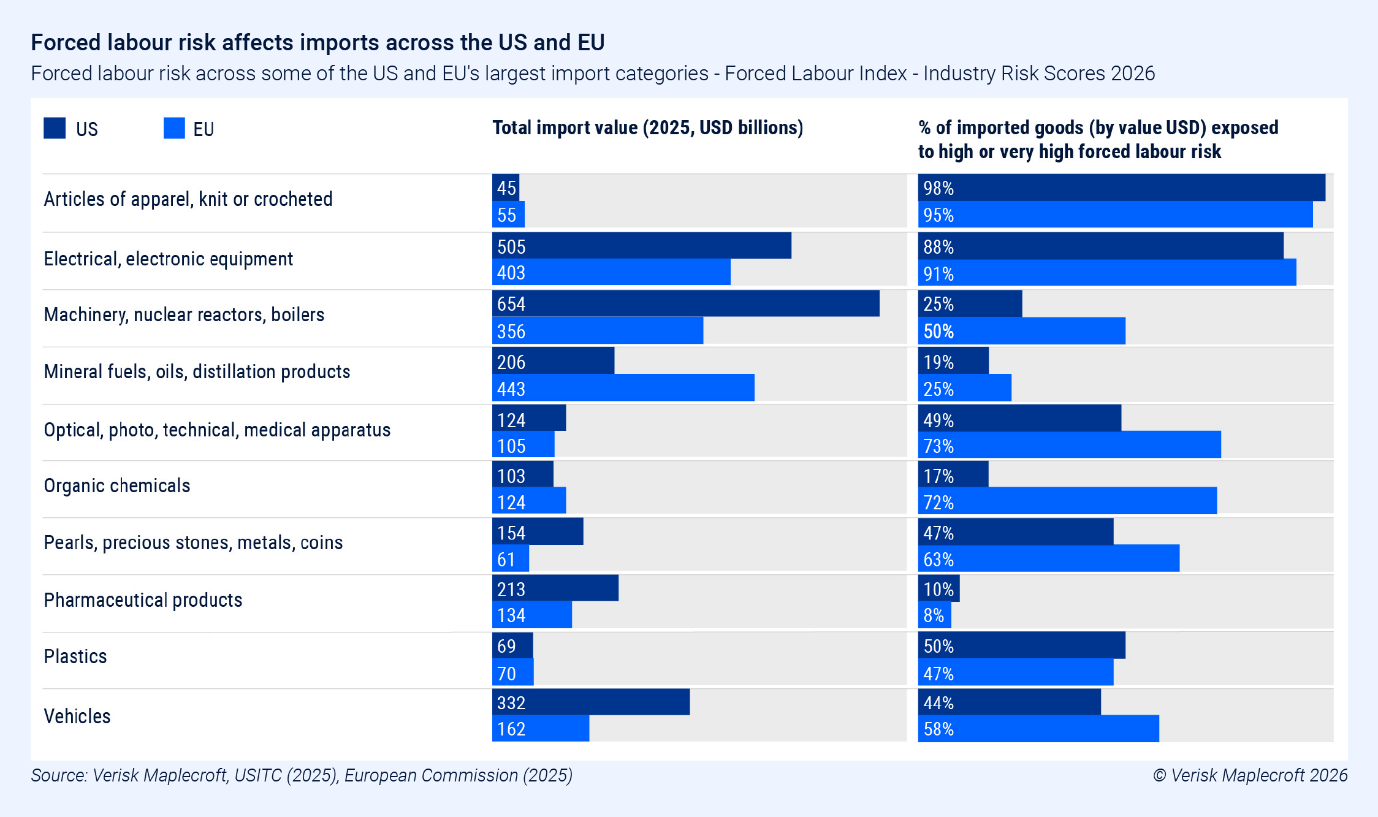

More than US$1tn of US imports and an estimated US$903bn of EU imports face high or very forced labour risk.

Apparel is the sector most at risk of forced labour – 98% of US imports and 95% of EU imports come from countries where the risk of forced labour is ‘high’ or ‘very high’.

Electrical and electronic equipment also faces elevated risk in both the US and the EU.

The report covered several other supply chain risks, which it dubbed overall “the great supply chain squeeze”.

These risks included a 40% increase since 2021 in the number of countries rated ‘high’ or ‘very high’ risk on the firm’s conflict intensity index, increasing human rights-related exposure across supply chains.

Verisk Maplecroft also suggested potential opportunities for companies looking to diversify their supply chains, pinpointing a group of target countries.

These are Thailand, the Philippines, Argentina, Uruguay and Chile, all of which have “viable” risk profiles at present and are slated to see them improve.

Last month, Verisk Maplecroft found that trade resilience had deteriorated in 157 countries over the last five years.

In its analysis of the world’s 500 busiest ports and 50 busiest airports, approximately one third were found to be exposed to a ‘high’ or ‘very high’ risk of disruption from at least one threat, such as geopolitical risk and conflict, natural hazards and domestic security.